Average Homeowners Insurance Cost in Colorado Ranks Top 10 Highest

The average homeowners insurance cost Colorado homeowners pay are some of the highest in the nation, consistently ranking inside the top ten year after year. Residents of The Centennial State face higher costs, and there are several reasons for the increase. This includes the fact that Colorado is one of the most affected states when it comes to wildfires and fire damage is the most expensive claim for homeowner insurance companies to deal with.

Furthermore, the average cost of homeowners insurance in Colorado is rising for many different factors. For example, if you own a home that is worth $500,000, you can expect to pay higher premiums than a home that has a value of $300,000. There are also many personal factors and unique factors to your property that will come into play.

However, getting to know the averages in your area is a great way to determine whether or not you are overpaying for coverage, or even underpaying for coverage. While getting the lowest price is always important, you also don’t want to be left with inadequate protection and spend more out of pocket after a loss as a result.

Freedom Insurance Group helps you determine the best coverage for your needs and then find the right coverage at the lowest price available. Learn more about the cost of homeowners insurance in Colorado, how to use averages to your advantage, and what you can do to save money while protecting your home.

What Is the Average Cost of Homeowners Insurance in Colorado?

The average homeowners insurance in Colorado costs $1584 per year, a noticeably higher future than the $1428 per year the average American homeowner will spend.

Breaking down how your premium is calculated is a bit complex. However, there are some key takeaways that can help you make sense of how insurance carriers calculate your premium. Here are the core factors that affect your cost of homeowners insurance in Colorado:

- The age and location of your home are two of the largest factors. Your roof’s age is also a major subfactor that deserves attention. Older homes in areas with frequent claims will pay higher rates.

- It’s also important to take into consideration the building materials used to create your home. Nicer materials cost more to replace and insure.

- The number of coverages you need is going to affect your rates, along with your policy limits. More coverages and higher limits will cost more.

- Your claim’s history is an element and if you have more claims, expect higher rates.

- You’re also going to need to take into consideration your deductible. A higher deductible can lower your rates but you’ll have more out-of-pocket costs after a loss.

- Your home’s condition, particularly your roof, will affect costs. A home in worse condition is more likely to sustain additional damage and costs more to insure.

- Changing weather patterns and crime rates are also going to play a part in creating your homeowners insurance cost in Colorado. More severe weather and crime mean you’ll have to pay more to protect your home.

- Personal factors are important to remember as well. This can be anything from credit scores to potential risk factors on your property, such as owning a trampoline or pool.

Ultimately, the theme that carries throughout any factor that affects your premium is risk. The riskier your property is to insure, the more you’ll pay, and considering Colorado comes with pretty severe risks, you can see why home insurance costs are elevated.

Average Cost of Homeowners Insurance by Colorado City

Understanding the average homeowners insurance rates in Colorado is helpful, but cities vary and the factors affecting one part of the state may not fully apply to another. This is why we’ve broken Colorado homeowners insurance rates down according to your city:

|

City |

Average Cost |

|

Denver |

$2,103 |

|

Colorado Springs |

$2,210 |

|

Aurora |

$1,495 |

|

Fort Collins |

$1,499 |

|

Lakewood |

$1,896 |

|

Thornton |

$2,001 |

|

Arvada |

$1,867 |

|

Westminister |

$1,657 |

|

Pueblo |

$2,305 |

|

Greenley |

$1,762 |

|

Centennial |

$1,993 |

|

City |

Average Cost |

|

Boulder |

$1,947 |

|

Lovemont |

$1,459 |

|

Loveland |

$1,584 |

|

Castle Rock |

$1,848 |

|

Broomfield |

$1,495 |

|

Grand Junction |

$1,567 |

|

Commerce City |

$1,855 |

|

Parker |

$1,694 |

|

Littleton |

$1,905 |

The 20 largest cities above represent the largest in Colorado by population.

Keep in mind that the above are only averages and even within cities, there are several things that may affect the amount you’ll pay. But there is a lot that we can learn by looking at averages within individual cities:

- If you’re paying much more than the average in your area, then it’s important to evaluate your coverage. On average, homeowners should assess their premiums at least once or twice a year and if you’re overpaying, you’ll need to shop for a better price.

- Alternatively, being far under the average in your city may mean you don’t have enough coverage. Lacking coverage can expose you to expensive losses which you’ll need to cover to restore your home.

Working with a licensed insurance agent can help you assess your needs, where you stand, and how to ensure you are staying protected without losing money today or tomorrow.

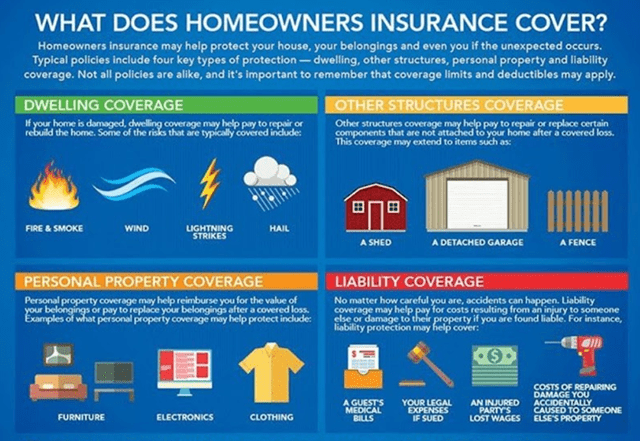

Basic Coverages Affecting the Average Cost of Homeowners Insurance in Colorado

Colorado Home Insurance Rates and Weather

Every state deals with its own form of severe weather, but none quite Colorado. Wind and hail damage continues to be the most common claim for homeowners and represents the third most expensive claim, averaging well over $11,000.

Additionally, there are around 320,000 homes at risk of wildfire damage in Colorado. This represents the third most homes at risk for extreme wildfires in the country. Remember, fire damage claims may not be the most frequent, but they average over $77,000 and are the most expensive claim you can make.

There are also flooding risks to consider. Wildfires and urban development have transformed the state of Colorado and made it more difficult for rainwater to settle into the ground. This has made flooding a growing concern for homeowners in The Centennial State. While flooding isn’t covered by your home insurance coverage, you’ll need a flood insurance policy, it still presents a risk of damage and it will affect how much you pay for your coverage.

Some of the factors that go into the home insurance cost Colorado homeowners will pay boils down to personal factors, but there isn’t anything you can do about the weather. Nevertheless, no matter what factors you are facing, there are ways to lower your monthly premium while maintaining the coverage you deserve.

How To Lower Your Average Homeowners Insurance Cost in Colorado

Lowering your premiums is possible for homeowners and there are several ways to do so. There are obvious and not-so-obvious methods that are at your disposal. Here are the best ways to lower the average cost of homeowners insurance in Colorado for your home:

Compare Multiple Home Insurance Carriers

The biggest tool in your arsenal is going to be comparing various carriers against each other. Beyond looking at the various risk factors that affect your premium, each carrier does so differently. This means that while they may be looking at similar factors, they are also weighing their risks differently. The result is different prices for the same coverage at the same home. Which is why it’s important to shop around.

Bundle Your Home and Auto Insurance

When you combined your home insurance with auto insurance in Colorado, you’ll receive a discount as a result. Carriers love rewarding customers that purchase multiple policies and do so often through bundles that provide necessary coverage at a lower rate.

Search For Discounts

Brands are looking to attract clients and there are various discounts available as ways to do so. You aren’t going to qualify for everything, but you may be able to qualify for some discounts, and every dollar counts. Furthermore, when you bundle, you can also access a variety of auto insurance discounts for even more savings.

Choose a Higher Deductible

Higher deductibles are a great way to save on your monthly premium. Just be sure that you are comfortable with your finances to pay larger out-of-pocket expenses following a loss. Remember, reimbursement for your claim only comes after you pay your deductible, meaning a higher deductible should be carefully considered.

Review Your Coverage

Not reviewing your coverage is a great way to leave money on the table. Lifestyles change as do factors in your area and the insurance market as a whole. You may face increases and only find out far too late leaving you with an unfavorable premium for another year. At least once a year, be sure to check on your policy’s premiums to see if they are still in line with your budget.

Control What You Can Control

You may not be able to control whether or not a hailstorm passes over your home, but you can control things such as your credit score or unnecessary claims. If you do your part, you can affect how much you pay through simple personal choices that improve your finances.

Implement Home Improvements

Certain home improvements can help you lower your premiums, such as smoke detectors, security systems, fire alarms, new roofing, etc. Overall, if it revolves around safety or helping the integrity of your home, it may be worth speaking with your insurance agent to determine if there are discounts available.

Lowering the cost of your coverage has many different paths and here at Freedom Insurance Group, our agents are here to help you find the best options available.

Since 2005, we’ve been helping homeowners identify the protection they need, compare their options among top-rated insurance carriers, and save money by pinpointing the lowest coverage available.

To get a quote for your home and to compare it with the average homeowners insurance in Colorado, give us a call today. You can also receive a free, no-obligation homeowners insurance quote by filling out our online form.