Commercial Truck Insurance in Missouri – Coverage, Quotes, and Filing

Summary:The right commercial truck insurance is essential in Missouri, not only as a requirement but as a means of protecting your enterprise. From owner-operators to fleets, it’s smart to compare quotes and customize your coverage. Different carriers assess risks differently, so shop around for the best fit. Whether you're hauling locally or across state lines, the right policy keeps your business rolling—and compliant—no matter what the road throws your way. Estimated Read Time: 15 mins

Table of Contents:

Running an enterprise often means running around, and when your fleet is on the road, how you’re protected matters. Commercial truck insurance is mandatory in Missouri, but if you only protect your vehicles with the bare minimum, you could be exposing your enterprise to many risks. Learn more, compare quotes, and find the right commercial policy no matter what your trucking endeavors require.

Commercial Truck Insurance Quotes in Missouri

With so many different industries and types of trucks available, it’s important to have coverage that fits your needs and budget. Compare commercial truck insurance quotes from top-rated companies in Missouri by using the tool below or by giving us a call at the number at the top of the page.

Keep in mind that each carrier looks at risk differently and will assess your coverage accordingly. In other words, no two companies look at your insurance the same.

As a result, you can expect to receive different premiums from different carriers. It’s critical to compare the quotes of multiple carriers to ensure you’re receiving the best protection at the lowest cost.

Who Needs Commercial Truck Insurance in Missouri?

Many different businesses rely on insurance for commercial trucks, and while there are a lot of different coverages to meet the diverse needs of different industries, everyone from owner-operators to enterprises with large fleets can benefit:

Owner-Operators

Owner-operator insurance protects truck drivers who own and operate their own rigs. Independent operators need liability, physical damage, cargo, and general liability coverage.

Those leased to a motor carrier may get primary liability, but often need additional coverage like non-trucking liability or trailer interchange. Commercial insurance for trucking is complex, and costs vary based on business type, truck, and driving history.

Motor Carriers (For-Hire Trucking)

For-hire trucking businesses have liability risks ranging from physical damage to medical bills and more. As an independent contractor, your motor carrier’s authority may provide extra coverage, such as non-trucking liability, however, there are additional coverages available to better customize your protection to meet your company’s specific needs.

Private Carriers

Private carrier insurance covers truckers hauling goods for their own company. Liability coverage is required, while optional coverages like physical damage and medical payments provide extra protection.

If you cross state lines, you may need federal or state insurance filings, but regardless, always ensure that the commercial truck insurance company you enroll with covers your risks and ensures all necessary paperwork is in order to keep you compliant and on the road.

What Does Commercial Trucking Insurance Cover in Missouri?

Having liability coverage is mandatory just in case you or your driver causes damage or bodily injury to another party. However, commercial truck insurance can cover a lot of different risks, including your own fleet, your cargo, rentals after an accident, and much more.

A commercial trucking insurance policy operates similarly to any other auto insurance, but protects against the specific risks larger trucks face every day.

This means no matter if a business or large, an owner-operator, or any other enterprise, you’re covered for what may come your way.

Because there are so many different industries and perils facing companies in Missouri, owners should find policies that best cover the specific risks of their business. Below are popular coverages protecting trucks in the Show Me State:

Liability

Liability coverage is required for anyone with commercial insurance for trucks but unlike other auto policies, the minimum requirements set by Missouri will vary due to a number of factors. This includes how many passengers your truck fits, the cargo you’re hauling, and the weight of your vehicle:

- Household Goods (Non-Hazardous): $100,000 for injury or death of one person, $300,000 for one accident, and $50,000 for property damage for one accident

- Passengers (12 or Fewer)*: $100,000 for injury or death of one person, $300,000 for one accident, and $50,000 for property damage for one accident

- Passengers (Over 12)*: $100,000 for injury or death of one person, $500,000 for one accident, and $50,000 for property damage for one accident

- Hazardous Materials (Bulk Only – GVWR of 10,0001 pounds or more)*: $1,000,000 in coverage for bodily injury and property damage

- Hazardous Materials (GVWR of 10,001 pounds or more)**: $5,000,000 in coverage for bodily injury and property damage

- Hazardous Materials (GVWR less than 10,001 pounds)**: $5,000,000 in coverage for bodily injury and property damage

If you’re traveling intrastate and carrying non-hazardous freight, the weight of your truck also matters. For trucks under 10,001 lbs, at least $300,000 in liability insurance must be carried. Vehicles weighing more than 10,001 lbs must maintain a minimum of $750,000 in liability coverage.

*Drivers are required to maintain $1.5 million worth of CSL coverage if they have 15 passengers or fewer, and those with 16 or more passengers must maintain $5 million worth of CSL coverage when travelling interstate.

**MoDOT has plenty of detailed regulations that may also require certain insurance minimums not listed here. To learn more, click the link to better understand Missouri’s Intrastate Operating Authority Insurance Requirements.

Uninsured/Underinsured Motorists

It might be a hit and run, or it could simply be someone who doesn’t have a policy. In some cases, drivers do carry insurance, but they don’t have enough coverage to restore your loss.

Especially when it comes to commercial trucks, the cost of repairs can easily exceed the policy limits of non-commercial drivers. UM/UIM coverage helps you avoid unnecessary expenses caused by others.

Trucks in Missouri are required to carry a minimum of $25,000 per person and $50,000 per accident for bodily injury in uninsured coverage, while underinsured protection is optional.

Comprehensive and Collision

Your truck is one of your biggest investments, so protecting it from accidents, theft, or natural disasters is a top priority. Collision coverage pays for damages from crashes, while comprehensive insurance covers non-collision incidents like fire, vandalism, or falling objects.

Motor Truck Cargo

Motor truck cargo insurance keeps your business covered when hauling goods. It protects your cargo from damage, theft, or loss caused by accidents and other unexpected events. Stay protected on the road and ensure your shipments arrive safely with the right coverage for your trucking business.

Non-Trucking Liability

There are times when you’re off the job, but issues may arise. For leased drivers, non-trucking liability insurance adds an extra layer of protection when you’re driving your truck for personal use. Should an accident occur during this period, even though you’re not under dispatch, your finances remain protected.

Trailer Interchange

If you haul trailers owned by others under a trailer interchange agreement, you need specific coverage to be protected from perils. Businesses with trailer interchange coverage are protected against damage or loss to the trailer while it’s in their care.

Medical Payments

Accidents can happen, and medical costs can add up fast. Protect your business from costly medical expenses for you and your passengers, regardless of who is at fault, with coverage for medical payments.

General Liability for Truckers

The risks of liability don’t just happen on the road. Having general liability insurance bolsters your commercial trucking policy to include protection for the non-driving incidents, your business might be held liable for. One example would be causing damage to someone’s loading dock, or if you delivery driver drops off the wrong items to your client.

Heavy Truck Roadside Assistance

The last thing any business wants to deal with is having a truck on the side of the road in need of repair. Sadly, it’s a part of operating. However, when breakdowns do happen, having roadside assistance can help you get back on the road sooner. Everything from minor repairs to jumpstarts to fuel delivery to tire changes and even locksmith services is covered.

Rental Reimbursement With Downtime

Rental reimbursement with downtime coverage helps keep your trucking business moving if your truck is out of commission due to a covered accident. Your policy covers the cost of renting a temporary replacement or provides financial support for lost income while your truck is being repaired.

This coverage is essential for truckers who rely on their vehicles for income, ensuring minimal disruption to operations and helping them stay on the road without major financial setbacks.

Gap Insurance

Gap insurance covers the difference between your truck’s loan balance and its actual cash value if totaled. Adding this coverage to your commercial trucking insurance policy can help you overcome paying for a loss cost.

Industry-Specific Coverages

Since trucks do a lot for us, it’s only right that we have multiple options to protect them. The risks of a big rig hauling logging cargo aren’t going to be the same as a tanker in the oilfield. Basically, if you have a specific commercial trucking insurance risk, we’re here to help you tailor your coverage as needed.

The Types of Vehicles Covered by Commercial Insurance for Trucks in Missouri

Finding the right commercial truck fleet insurance or even coverage for an individual vehicle comes down to determining which type of machine you’re operating.

There are different regulations and coverages available depending on the operations your business conducts.

Overall, this allows business owners to make an informed decision and choose coverage that protects against their industry’s specific risks.

Agricultural Trucks

Farmers and agricultural businesses in Missouri rely on a range of trucks to transport goods, equipment, and supplies efficiently. Large agricultural trucks haul heavy machinery like tractors and combines, while smaller ones move bales of hay, grain, or water barrels.

Tractors handle everything from plowing to towing, while combine harvesters make grain harvesting faster. ATVs and UTVs help workers navigate fields quickly. Other essential vehicles include balers for hay, spreaders for fertilizers, and sprayers for pesticides—each playing a vital role in farming operations.

Regardless of the equipment, keeping your farm operational, there are coverage options available that provide specific protections for the risks at hand.

Box Trucks

Box truck insurance protects businesses using these trucks for deliveries or services, covering accidents, liability, and vehicle damage. Whether you're a private carrier or a for-hire trucker, policies can be customized to include liability, cargo protection, and physical damage coverage. Costs depend on the size of your truck, what you’re carrying, and your driving history.

Bucket Trucks (Cherry Pickers)

Bucket truck insurance safeguards your business from financial risks like accidents, theft, vandalism, or weather damage. These specialized vehicles are a major investment, and the right coverage helps avoid costly out-of-pocket repairs. It also protects against the unique risks cherry pickers face on the job.

Car Carriers (Rollbacks)

Car carrier truck insurance protects businesses transporting vehicles from accidents, damage, and liability risks. Policies cover open and enclosed trailers, ensuring financial protection for multi-level haulers, flatbeds, and roll-back carriers. Given the high value of the cargo being transported, coverage often includes collision, cargo insurance, and liability.

Catering Trucks

Operating a catering truck in Missouri? You’ll need commercial auto insurance to cover accidents and vehicle damage. General liability protects against customer injuries or property damage, while workers’ comp is essential if you have employees.

Keep in mind that some cities may require additional coverage, like product liability for food-related risks. Always stay up to date on local regulations to ensure you have the right coverage for your service area.

Cement Mixers

If you’re operating a cement mixer truck, Missouri requires liability insurance, but the amount of coverage depends on how much your vehicle weighs and the cargo inside. Additionally, if you’re hauling hazardous materials, FMCSA rules may require higher limits, and finally, cargo insurance might also be necessary, as Missouri mandates minimum coverage, which will vary depending on where you are operating.

Dump Trucks

Dump truck operators in Missouri must have commercial insurance, with at least $750,000 in liability coverage, however, $1 million in coverage is often recommended. These heavy trucks pose significant risks, making proper coverage essential throughout the construction, landscaping, and waste management industries that rely on them daily.

Personal-use dump trucks may be exempt from the rules of the DOT, but they still need to meet basic insurance requirements.

Food Trucks

If you own a food truck, the right insurance keeps your focus on your culinary creations while your business keeps rolling safely. From customer illness to property damage and employee injuries, the coverage protects you from unexpected risks.

Costs vary based on what you serve, and having certain equipment, such as grills and fryers, will add extra risks. Whether you're the neighborhood ice cream truck or are serving fusion tacos, the right policy will be there for you when you need it.

Flatbeds

Operating flatbed trucks in Missouri requires coverage between $750,000 and $5 million due to DOT regulations. This varies depending on what you're hauling, and if you don't have the right commercial truck insurance, you can face fines and legal issues.

Front Loaders

If your business relies on front loaders, the right commercial truck insurance is a must. These machines handle heavy lifting in construction, mining, agriculture, waste management, and even snow removal. Whether you're using backhoe, skid steer, or track-type loaders, proper coverage protects against accidents, damage, and liability.

Garbage Trucks

The risks of waste removal range from severe damage caused by accidents, medical bills for staff loading and operating the trucks, as well as liability, and potential damage outside of a traditional accident. Just like any other venture, having the right commercial truck insurance is the key to staying protected.

Pump Trucks

Pump trucks are essential for construction, cleanup, and the oil industry, but they come with big risks. These heavy-duty trucks are valuable assets, yet accidents, spills, or hazardous materials can lead to costly liabilities. Some sewer trucks may even require higher insurance limits due to potential contaminants. Protecting your pump truck with the right insurance ensures your business stays covered against unexpected events while keeping operations running smoothly.

Refrigerated Trucks

Refrigerated truck insurance goes beyond basic auto liability, covering risks like collisions, theft, vandalism, and fire. It can also include medical payments for drivers, uninsured motorist protection, and cargo insurance for perishable goods. Additional options like towing, storage, and specialized refrigeration unit coverage help keep your business protected.

Stake Body Trucks

Stake body truck insurance protects your business from unexpected costs like accidents, cargo damage, or theft. These trucks haul everything from lumber to heavy equipment, so the right coverage is essential. Protect your vehicle, cargo, and liability risks with a customized policy that keeps your business running smoothly.

Street Sweepers

Insurance is a crucial part of running a street sweeper company, protecting your business from costly risks. General liability covers accidents, injuries, and lawsuits, while pollution liability coverage is also available due to the nature of cleaning dirty streets. Property insurance is available to safeguard your equipment, and umbrella policies provide extra protection.

With street sweepers operating in public spaces and costing hundreds of thousands, the right coverage ensures your business stays secure while dealing with diverse risks in a variety of environments.

Tank Trucks

Tank truck insurance is a must-have for businesses hauling liquids, gases, or hazardous materials. It covers accidents, spills, and liability risks unique to these specialized trucks.

Since tankers carry high-risk cargo, policies often include hazmat coverage, pollution liability, and increased limits. Whether you own one truck or a fleet, having the right insurance ensures compliance, protects your assets, and keeps your business running smoothly.

Tow Trucks

Running a tow truck business comes with risks like accidents and vehicle damage, but well-rounded coverage is going to include more than just the bare minimum. Essential insurance includes liability, but also adds important considerations like protection for on-hook towing and garagekeepers coverage. The right policy keeps your business running smoothly and prevents financial setbacks from everyday perils your company faces while operating.

Finding Insurance for Commercial Truck and Filing in Missouri

If you operate a motor carrier in Missouri, you must have the proper insurance on file at all times. This includes a surety bond or a public liability and property damage insurance certificate that meets state requirements.

When transporting household goods within Missouri, cargo insurance is also required unless the shipper agrees otherwise in writing.

All insurance filings must be submitted electronically through MoDOT Carrier Express, with limited exceptions for faxed or mailed copies.

The Missouri Department of Transportation must be listed as the filing agency, and your insurance provider must be authorized to do business in the state.

Documents must be legible, properly signed, and meet all state guidelines. Without the right coverage in place, your business could face legal and financial risks.

Ensure your policy meets Missouri’s requirements to keep your trucks on the road and your business in compliance:

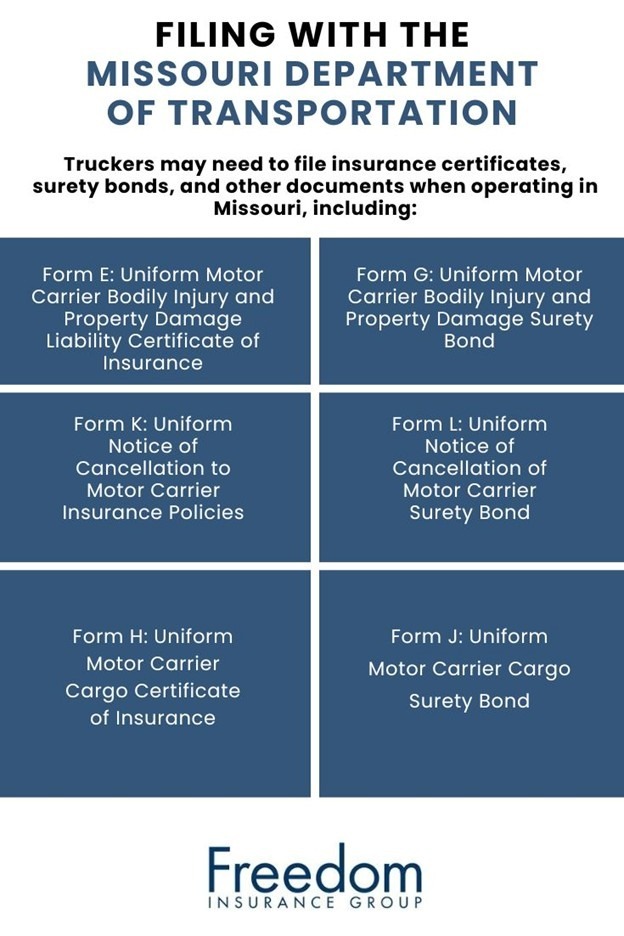

- Motor carriers in Missouri must provide proof of insurance using specific forms. Liability coverage requires either Form E (Motor Carrier Bodily Injury & Property Damage Liability Certificate) or Form G (Uniform Motor Carrier Bodily Injury and Property Damage Surety Bond). If a policy is canceled, insurers must submit at least 10 days' notice using Form K (for Uniform Notice of Cancellation to Motor Carrier Insurance Policies) or Form L (for Uniform Notice of Cancellation of Motor Carrier Surety Bonds).

- For cargo insurance, carriers are required to file either Form H (Motor Carrier Cargo Certificate of Insurance) or Form J (Uniform Motor Carrier Cargo Surety Bond). The amount of liability coverage you carry varies based on the goods being shipped, the number of passengers, etc., as stated above.

- Hazardous material involves stricter liability requirements and requires filing Form E or Form G to ensure compliance with federal and state regulations.

When you buy commercial truck insurance, some carriers help with the paperwork required to stay compliant with state and federal laws, especially in Missouri.

After you apply for trucking authority, your insurer can handle key filings like the ICC MCS-90 (for federal liability proof), Form E, and Form H. If needed, they may also handle SR-22 forms for high-risk drivers.

These filings prove you have the proper insurance in place to operate legally, so you don’t have to worry about missing a step. It’s all about making sure your business is protected and road-ready without the hassle.

Once you’ve got your policy and authority in place, your insurance provider may be able to take care of the rest, keeping you focused on running your business, not chasing paperwork.

Whether you're hauling cargo across state lines or operating locally, staying compliant is easier when your insurance team handles the filings for you.

How to Save on Boat Insurance in Missouri

You can easily save on coverage for your watercraft, as many insurers offer discounts for safe boating, homeownership, multiple boats, paying in full, taking a Missouri-approved safety course, or bundling policies.

Bundling boat insurance with another policy can lower costs, but it’s not always the best deal, and while discounts are appealing, separate boat insurance might offer better coverage for a lower price.

The best thing boaters can do is shop around to ensure that they are receiving the best coverage at the lowest cost.

To compare Missouri boat insurance policies, give us a call at the number above for a free personalized quote from top-rated carriers near you.