Commercial Truck Insurance in Tennessee

Summary: Getting the right commercial truck insurance in Tennessee isn’t just a legal requirement; it’s a smart move to protect your business. Whether you’re an owner-operator or managing a fleet, comparing quotes and customizing coverage is key. Since insurers evaluate risk differently, shopping around helps you find the best fit. No matter where the road takes you, including local routes or out-of-state hauls, the right policy keeps your business covered and compliant Estimated Read Time: 13 mins

Table of Contents:

Tennessee commercial truck insurance is there for small businesses when they need help for their fleet the most. It doesn’t matter what your industry is, risk factors, or if you’re managing a single vehicle or twenty, there’s coverage available to meet your needs. Learn more about how to find cheap commercial truck insurance, compare quotes, and find the right fit that meets the needs of your enterprise.

Tennessee Commercial Truck Insurance Quotes

With a wide range of trucks and industries out there, it's essential to find commercial truck insurance that matches your company's specific needs and budget.

Use the tool below or call the number at the top of the page to compare commercial truck insurance quotes from top-rated providers in Tennessee near you:

While top-rated commercial truck insurance companies are more than capable of protecting your business, their premiums will vary. Each carrier determines risk differently, and as a result, you’ll find differing premiums.

This is why it’s always advised to compare multiple commercial trucking insurance quotes from different carriers to find the lowest possible cost for the protection your enterprise needs to keep moving forward after suffering a loss.

Who Needs Commercial Truck Insurance in Tennessee?

If you’re operating a truck for business purposes in the state of Tennessee, you’re going to need coverage to stay compliant.

Commercial insurance for trucks is required by law and also provides important protections that keep your business from having to pay out of pocket when things go wrong. It’s a specific type of commercial auto insurance that is tailored to the perils trucking operations face day in and day out.

From large enterprises managing a fleet of trucks to owner-operators hotshotting across the state and everyone in between, commercial truck insurance in Tennessee benefits a wide variety of businesses across a variety of industries.

Owner-Operators

Owner-operator insurance covers truckers who run their own rigs. Independent drivers need commercial insurance for trucking, which provides protection for liability, physical damage, cargo, and more.

If leased to a carrier, you might have primary liability, but still need extras like non-trucking liability or trailer interchange. However, coverage needs vary by truck type, business model, and driving record.

Motor Carriers (For-Hire Trucking)

For-hire trucking businesses face risks like physical damage and medical costs. While a motor carrier may offer some coverage, independent contractors can add policies, like non-trucking liability, to tailor protection to their specific needs.

Private Carriers

Private carrier insurance protects truckers who haul goods for their own business. Liability coverage is required, while optional add-ons like physical damage and medical payments offer added security. If you cross state lines, you may need specific federal or state filings, so it’s important to find commercial insurance for your truck that covers your risks and keeps you compliant.

What Does Commercial Trucking Insurance Cover in Tennessee?

Liability coverage is a must in case your driver causes damage or injury, but commercial truck insurance in Tennessee can do so much more.

Your policy can also cover your fleet, cargo, rentals, and many other perils specific to your company's operations.

Commercial truck coverage works like regular auto insurance but is built for the unique risks trucks face every day. Whether you’re a solo operator or running a large business, having the right protection matters.

Understanding the difference between interstate and intrastate coverage is essential in the trucking industry:

- Interstate Coverage is required for motor carriers transporting goods across state lines. It usually comes with higher insurance limits due to the increased risks. Intrastate coverage applies to transporting goods within a single state and typically has lower limits.

- Intrastate Coverage requires carriers hauling hazardous materials to follow additional regulations.

To operate legally, trucking businesses must meet specific insurance requirements set by the Federal Motor Carrier Safety Administration (FMCSA). These include:

- Minimum Coverage: FMCSA requires different coverage amounts based on the type of cargo. Non-hazardous freight under 10,001 pounds requires $300,000 in coverage, while freight over 10,001 pounds needs $750,000. For hazardous materials, coverage ranges from $1,000,000 to $5,000,000, depending on the material.

- CDL Requirements: A Commercial Driver's License (CDL) is needed if you're hauling over 26,000 pounds.

- MC and DOT Authority: To operate, you need a Motor Carrier (MC) number for interstate operations and may need to register with the state’s Department of Transportation (DOT) for intrastate.

- Vehicle Information: When applying for insurance, you'll need to provide details about each vehicle, including make, model, year, and VIN.

Liability

Everyone has to have liability coverage, especially commercial truck, but for businesses, policies work a little differently. Remember, the amount of coverage you’ll need depends on your truck’s weight, cargo, etc.

Comprehensive and Collision

Protecting yourself from liability claims is important but there are several additional risks your truck might face both during and outside of an accident:

- Having comprehensive coverage keeps your business covered for things like hail damage, trees falling on your vehicle, wildfires, vandalism, etc.

- Collision coverage is there to help you restore your truck after an accident.

Keep in mind that while both coverages reimburse you, bearing most of the financial burden for your business, you must first pay a deductible when filing a claim.

Uninsured/Underinsured Motorists

Whether it’s a hit-and-run or an underinsured driver, UM/UIM coverage protects you from paying out-of-pocket when the other party can’t cover the damage, especially important for costly commercial truck repairs.

Motor Truck Cargo

Motor truck cargo insurance safeguards the goods you transport, covering losses from theft, damage, or unforeseen incidents. It helps protect your business from financial setbacks and ensures your freight is covered every mile of the journey. With the right policy, you can deliver with confidence, knowing your cargo is secure.

Non-Trucking Liability

Even when you’re off the clock, accidents can happen. Non-trucking liability insurance provides coverage for leased drivers using their truck for personal reasons. If you're not under dispatch and an accident occurs, this policy helps cover damages, offering peace of mind and financial protection when you're not on the job.

General Liability for Truckers

Liability risks don’t end when the wheels stop turning. General liability insurance extends your coverage to include non-driving incidents your business could be held responsible for, such as damage to a client’s loading dock or delivering the wrong items. It’s a valuable safeguard that complements your core commercial trucking policy.

Trailer Interchange

If you’re hauling trailers under a trailer interchange agreement, you’ll need dedicated coverage. Trailer interchange insurance protects you from damage or loss to a trailer while it’s in your possession, even if you don’t own it.

Medical Payments

Accidents are unpredictable, and medical bills can pile up quickly. Medical payments coverage helps safeguard your business by covering healthcare costs for you and your passengers, no matter who’s at fault.

Heavy Truck Roadside Assistance

Breakdowns are an unavoidable part of running a trucking business, but roadside assistance can make them less stressful. From jumpstarts and fuel delivery to tire changes, minor repairs, and even locksmith services, this coverage helps get your truck back on the road quickly.

Rental Reimbursement With Downtime

Rental reimbursement with downtime coverage helps keep your business running when your truck is in the shop after a covered accident. Your policy can pay for a rental or cover lost income, reducing financial strain and keeping operations on track.

Gap Insurance

If your truck is totaled but it’s not paid off, your company is still going to have its note as an expense. Instead of paying for a vehicle you can no longer use, gap insurance covers the difference between the loan balance and the actual cash value (ACV) if totaled, to take this off your plate.

Industry-Specific Coverages

The risks of a dedicated deliveries carrying vital healthcare cargo are different than hauling oversized equipment for a manufacturing plant. No matter what risks you’re facing, commercial trucking insurance coverages are available to help you stay protected accordingly.

The Types of Vehicles Covered by Commercial Insurance for Trucks in Tennessee

Choosing the right trucking commercial insurance policy depends on the type of vehicle and how it’s used. Different operations have different rules, risks, and needs. Understanding these helps business owners pick a policy that protects against the unique risks of their enterprise.

Agricultural Trucks

Agriculture is one of the biggest industries in the Volunteer State, and Tennessee farmers use various trucks and equipment to keep operations running smoothly. From large trucks hauling tractors and combines to smaller ones moving hay, grain, or supplies, it takes a mix of vehicles to put food on the table.

Tractors plow and tow, while combines speed up harvesting. ATVs, UTVs, balers, spreaders, and sprayers all serve vital roles. No matter the vehicle, there are commercial insurance options designed to protect your farm from the unique risks each one carries.

Box Trucks

Box truck insurance covers accidents, liability, and vehicle damage for businesses using these trucks for deliveries or services. Whether you're a private carrier or work for hire, you can tailor coverage to include cargo protection and physical damage. Costs vary based on truck size, cargo type, driving history, and industry.

Bucket Trucks (Cherry Pickers)

Bucket truck insurance protects your business from costly risks like accidents, theft, and weather damage. These high-value vehicles face unique on-the-job hazards, and the right coverage helps avoid expensive repairs and keeps your operations running smoothly.

Car Carriers (Rollbacks)

Car carrier truck insurance protects businesses that transport vehicles from accidents, damage, and liability. It covers both open and enclosed trailers, including flatbeds and roll-backs. With high-value cargo, coverage typically includes liability, collision, and cargo insurance for full financial protection.

Catering Trucks

Operating a catering truck in Tennessee requires the right insurance from the start. Commercial truck coverage handles accidents and vehicle damage, while general liability protects against customer injuries or property damage. If you have employees, workers’ compensation is essential.

Some cities may also require additional coverage, such as product liability for food-related risks. Staying up to date on local regulations ensures your policy meets all legal requirements.

Cement Mixers

Cement mixer truck operators in Tennessee must carry liability insurance, with coverage amounts based on the truck’s weight and cargo. Federal rules require higher limits if you're transporting hazardous materials, so more coverage is needed. Furthermore, cargo insurance is often needed, too, as Tennessee requires different minimum coverages, depending on your operating location.

Dump Trucks

Dump truck operators in Tennessee need commercial insurance with at least $750,000 in liability, though $1 million is often recommended. These high-risk vehicles are vital in construction, landscaping, and waste industries. Remember, even personal-use dump trucks must meet basic coverage requirements.

Food Trucks

Food truck insurance helps you stay focused on serving great food while protecting your business from unexpected risks. It covers things like customer illness, property damage, and employee injuries. Costs depend on what you serve and your equipment, with grills and fryers bringing higher risks. Whether you run an ice cream truck or serve fusion tacos, the right policy keeps your business rolling.

Note: Keep in mind that different cities may have different requirements. For example, Nashville’s popular food truck scene may follow certain regulations and require coverage different from those found in a rural market. Working with an agent can help your business avoid pitfalls, coverage gaps, and compliance issues.

Flatbeds

Flatbed hauling comes with higher risks, including theft, cargo claims, and the need for specialized handling. Insurance for commercial trucks typically excludes certain items like steel coils or machinery, and may deny claims for issues like damp cargo or driver negligence. Trucking companies should carefully review their policy and request broad form coverage to ensure proper protection.

Front Loaders

Front loaders play a vital role in industries like construction, agriculture, and waste management. Whether you're using a backhoe, skid steer, or track loader, commercial truck insurance is essential to protect against accidents, damage, and liability.

Garbage Trucks

Waste removal comes with unique risks—from accidents and equipment damage to medical costs and liability issues. Commercial truck policies help protect your business from these hazards and ensure operations stay on track.

Pump Trucks

Pump trucks play a key role in construction, cleanup, and oil work, but they carry serious risks. Accidents, spills, and hazardous materials can lead to expensive liabilities, especially for sewer trucks handling contaminants. The right trucking insurance protects your valuable equipment and keeps your business running when the unexpected happens.

Refrigerated Trucks

Refrigerated truck insurance covers more than standard auto liability, it protects against collisions, theft, vandalism, and fire. It can also include medical payments, uninsured motorist coverage, and cargo insurance for perishable goods. Add-ons like towing, storage, and refrigeration unit protection help keep your business running smoothly.

Semi Trucks

Insurance for semi trucks protects your drivers, trucks, and cargo from accidents, property damage, and liability claims. Whether you’re an owner-operator, motor carrier, or private carrier, having the right coverage helps keep your business legally compliant and financially secure. It’s essential for anyone operating semi trucks for business purposes.

Stake Body Trucks

Stake body truck insurance helps cover unexpected costs like accidents, cargo damage, or theft. These trucks often carry valuable loads like lumber or equipment, so the right coverage is key. A customized policy protects your vehicle, cargo, and liability, keeping your business moving without disruptions.

Street Sweepers

Insurance protects street sweeper companies from costly risks. General liability covers accidents and lawsuits, while pollution liability addresses cleanup-related exposures. Property insurance protects equipment, and umbrella policies offer added coverage. With expensive machines operating in public areas, the right policy keeps your business secure.

Tank Trucks

Tank truck insurance is essential for businesses hauling liquids, gases, or hazardous materials. It covers accidents, spills, and liability risks, often including hazmat and pollution coverage with higher limits.

It doesn’t matter if you’re operating only one truck or need commercial truck fleet insurance; the right policy ensures compliance, protects your assets, and keeps your business moving.

Tow Trucks

Tow truck businesses face unique risks, which is why basic liability typically isn’t enough. Enrolling in coverages specific to your operations, like on-hook towing and garagekeepers insurance, helps protect your vehicles, equipment, and customer property against a wider range of viable threats.

Finding Insurance for Commercial Truck and Filing in Tennessee

Starting or operating a trucking business in Tennessee involves a few key paperwork steps to ensure compliance with state regulations.

To operate legally in Tennessee, you must submit your forms via the Tennessee Taxpayer Access Point (TNTAP) account. Your mandatory documents include:

- Intrastate Authority Application: This form is necessary to establish your authority to operate within the state.

- Designated Agent for Service of Process Form: This assigns a Tennessee representative who can be served with legal documents on your behalf.

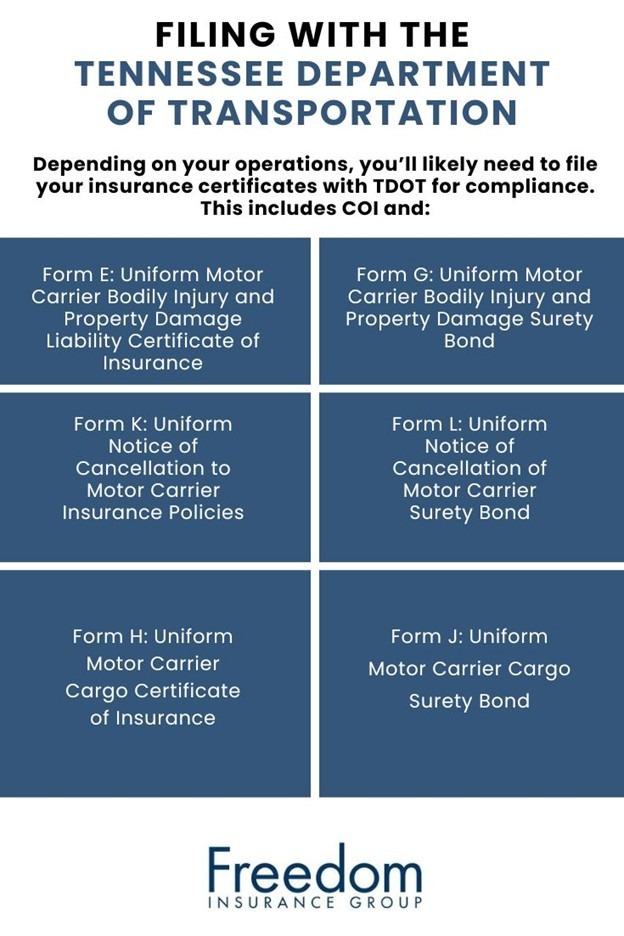

- Proof of Insurance: Commercial trucking coverage is a must, and the following forms should be submitted:

- Form E: Uniform Motor Carrier Bodily Injury and Property Damage Liability Certificate of Insurance.

- Form H: Uniform Motor Carrier Cargo Certificate of Insurance (required for carriers hauling general freight, household goods, or mobile homes).

- COI (Certificate of Liability Insurance): This proves you have the required coverage.

Depending on your business type, some forms are not mandatory but may be required based on the nature of your operations:

- Proof of Liability Insurance: Depending on the coverage you carry, you may need to submit either Form E or Form G (Uniform Motor Carrier Bodily Injury and Property Damage Surety Bond). If your insurance policy is canceled, Form K (Uniform Notice of Cancellation to Motor Carrier Insurance Policies) or Form L (Uniform Notice of Cancellation of Motor Carrier Surety Bonds) must be filed to notify the state.

- Cargo Insurance: If you're hauling cargo, you may need to provide Form H (Uniform Motor Carrier Cargo Insurance Endorsement) or Form J (Cargo Surety Bond). The specific form depends on the type of goods you're transporting.

- Hazardous Materials: If you’re hauling hazardous materials, stricter requirements apply, and you'll need to provide Form E or Form G to meet both state and federal regulations.

Navigating all these forms can seem overwhelming, but many commercial insurance companies help with the paperwork.

When you secure commercial truck insurance, your insurer can assist with filings like your ICC MCS-90 for federal liability proof, ensuring that you stay compliant. If needed, they can also handle SR-22 forms for high-risk drivers.

That means less time managing paperwork and more time focusing on your routes, customers, and business growth.

Once your authority is approved and your insurance is in place, your insurer can take care of the bulk of the filing, allowing you to focus on your business without the hassle of paperwork. This is especially helpful if you’re operating across state lines or within Tennessee.

In short, ensuring your trucking company’s compliance is key to operating legally and efficiently. With the right coverage and support, you can drive forward without worrying about the paperwork.