Save on Homeowners Insurance in Tennessee

Summary: Homeowners insurance in Tennessee protects against common risks like storms, theft, and fire, with costs averaging $900–$3,200 per year. Rates vary by city, home value, and personal factors. Comparing multiple carriers, exploring discounts, and customizing coverage with Freedom Insurance Group helps homeowners secure the best protection and price statewide. Estimated Read Time: 7 mins

Table of Contents:

- How Much Is Homeowners Insurance in Tennessee?

- Who Has the Best Homeowners Insurance in Tennessee?

- Types of Homeowners Insurance Coverage in Tennessee

- Home Insurance Discounts in Tennessee

- Is Homeowners Insurance Required in Tennessee?

- Do You Need Fire Insurance on Your Home in Tennessee?

- Get Help With Homeowners Insurance in Tennessee

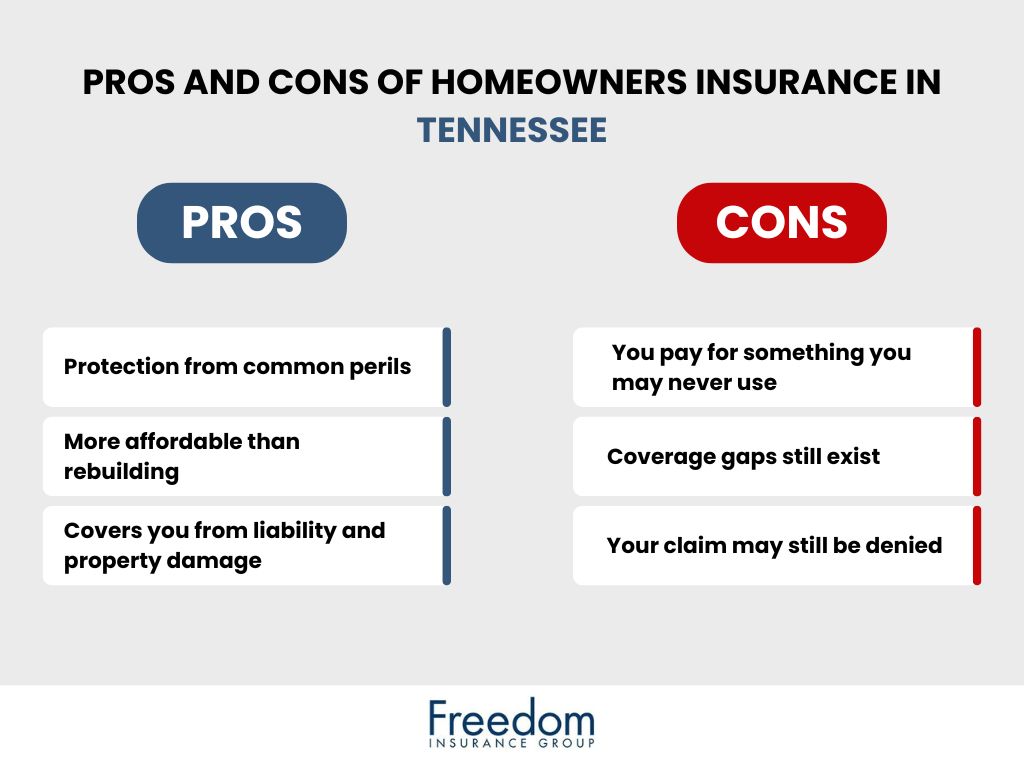

Homeowners insurance in Tennessee helps protect your biggest investment against risks like wind, hail, tornadoes, wildfires, and theft. With unpredictable weather and rising costs, having the right protection is essential.

But here’s the catch: the best homeowners insurance in Tennessee isn’t the same for everyone. Prices and coverage depend on your location, your home’s value, and even your personal claims history. That’s why shopping around is the only way to make sure you’re getting both reliable coverage and the lowest rate.

Our guide helps you compare averages, understand your coverage options, and you can even compare quotes using our tool below for a personalized approach to your premiums. Let’s take a closer look below as we break things down:

How Much Is Homeowners Insurance in Tennessee?

Homeowners insurance costs in Tennessee typically fall between $900 and $3,200 per year, running above the national average. It's a wide range depending on your home and other personal factors, but the higher rates stem from frequent severe weather and elevated claim activity across parts of the state.

Prices also fluctuate by location, so knowing the averages near your home is important, even if individual factors will affect your personal rate. Here’s a closer look at how much homeowners insurance in Tennessee costs on average:

Average Cost of Homeowners Insurance by City in Tennessee

| Rank | City / Metro Area | Typical Dwelling Coverage | Average Annual Cost |

|---|---|---|---|

| 1 | Morristown, TN | ≈ $250,000 | ≈ $1,548 |

| 2 | Kingsport, TN | ≈ $300,000 | ≈ $2,175 |

| 3 | Cleveland, TN | ≈ $300,000 | ≈ $2,680 |

| 4 | Knoxville, TN | ≈ $300,000 | ≈ $2,500 |

| 5 | Chattanooga, TN | ≈ $300,000 | ≈ $2,723 |

| 6 | Johnson City, TN | ≈ $300,000 | ≈ $2,465 |

| 7 | Jackson, TN | ≈ $300,000 | ≈ $3,555 |

| 8 | Nashville, TN | ≈ $300,000 | ≈ $2,023 |

| 9 | Clarksville, TN | ≈ $300,000 | ≈ $2,712 |

| 10 | Memphis, TN | ≈ $300,000 | ≈ $3,663 |

While Memphis and Jackson rank among the most expensive areas in the Volunteer State, smaller cities like Morristown are much more affordable.

Who Has the Best Homeowners Insurance in Tennessee?

There isn’t a single “best” carrier for everyone, as what is right for your needs may differ from that of someone who lives across town or even your neighbor.

The best homeowners insurance in Tennessee depends on your unique situation. Some companies excel in low rates, while others shine with customer service or bundling options.

Here are some tips for finding the right fit:

- Best for Low Rates: Often, regional carriers offer lower premiums than larger carriers.

- Best for Bundles: Using larger brands, such as Nationwide and Progressive, often unlocks savings by allowing families to bundle home and auto insurance.

- Best for Customer Service: Travelers and Amica Mutual earn strong satisfaction scores.

- Best for High-Value Homes: Chubb provides specialized coverage for luxury properties.

No matter what, you’ll never know what the best coverage or lowest rate is for your home unless you take the time to compare quotes from multiple companies. It takes less time than you think, and the savings are often substantial.

Types of Homeowners Insurance Coverage in Tennessee

A standard home insurance policy (HO3) offers residents multiple protections, including your home, but also extends to your other structures, personal property, and much more.

Here are the different coverages that make up your home insurance policy:

Dwelling Coverage

Your dwelling coverage holds the largest value within your policy as a whole. Its job is to protect your home’s structure (walls, roof, foundation, etc.) and any structure attached to your home as well.

You’re protected from various perils that may cause harm to your home, including fires, lightning, tornadoes, hail, accidental water damage/frozen pipes, vandalism, etc.

Protecting your home from such destructive forces is important, but the policy limits you set in your dwelling coverage also affect the rest of your policy.

It’s important to have enough coverage to fully rebuild your home after a total loss and to have adequate protection so that the rest of your policy has high enough policy limits for whatever might come your way.

Other Structures Coverage

Just like your home is protected from windstorms, hail, snowstorms, etc., so too are your sheds, detached garages, fences, etc. Other structures coverage helps complete your protection throughout your property.

Personal Property Coverage

When perils affect your home, your personal belongings are often subjected to damage as well. With personal property coverage, they receive the same protection as your home and other structures do during a loss.

It’s important to note that there are policy limits, and if you have single items or collections that are particularly valuable, you may need to increase your limits or add on endorsements that increase your protection.

Loss of Use Coverage

Loss of use coverage or additional living expenses protection provides you with coverage if your home is damaged so badly by a peril that it becomes uninhabitable, and you’ll need to live elsewhere.

You are provided with reimbursement for hotels, dining, and other related expenses while you are waiting for your home to be livable once again.

Personal Liability Coverage

Home insurance is important for many reasons, and one of them is the personal liability coverage it provides.

Should someone be injured on your property, you can cover their medical bill and your legal expenses if necessary.

Medical Payments to Others Coverage

Depending on the injury, you may need more protection, which is where Medical Payments to Others (Coverage F) comes in.

You’ll need to check your policy’s terms and conditions for more serious injuries; however, your home insurance policy will help you cover an injured party’s medical bills and potentially help you avoid legal issues.

Additional Optional Coverages

Tennessee home insurance policies deliver plenty of protection, but there are several things homeowners aren’t protected from that require additional coverage:

- Flood Insurance: The National Flood Insurance Program (NFIP) is available, along with private carriers, to help you protect yourself from damage. While homes are protected from many damaging weather events, flooding is not one of them.

- Homeowners Insurance Riders/Endorsements: There are several endorsements available that help you personalize your protection with affordable coverage not ordinarily covered by your policy. For example, you can add a rider that covers a particularly expensive piece of jewelry that your personal property coverage doesn’t have high enough policy limits for.

Home Insurance Discounts in Tennessee

You have plenty of options to save on the cost of home insurance through discounts.

Everyone needs to compare their coverage among multiple carriers to get the best rate, but it’s also important to look at the different discounts each carrier is offering as well.

Here are a few common discounts available to homeowners:

Home and Auto Bundles

If you own a home, chances are, you own a vehicle too. Bundling your home and auto insurance policies is a great way to save and consolidate the process for an easier experience.

Everyone who drives in Tennessee is required to have car insurance. Bundling these policies with your home insurance helps you protect against more while spending less.

New Home

Many carriers will give you a discount on homeowners insurance if you are purchasing a new home.

On average, newer homes come with fewer risks as they are less likely to have wear and tear, things break, or be affected by weather damage.

If you’re purchasing a new construction, be sure to ask about potential discounts with your agent to maximize your savings.

Increase Your Deductible

In most cases, if you pay a higher deductible, you’ll pay lower premiums as a result. Just remember that you’ll need to pay more after a loss before receiving your reimbursement following a claim.

Is Homeowners Insurance Required in Tennessee?

Tennessee law does not require homeowners insurance. However, mortgage lenders almost always do. Even without a loan, going without coverage is a major risk. One storm or fire could mean hundreds of thousands of dollars in damage without financial protection.

Do You Need Fire Insurance on Your Home in Tennessee?

Fire coverage is included in most standard home insurance policies. However, if you live in wildfire-prone areas like Sevier or Blount County, check for exclusions and consider endorsements that expand protection.

In 2022 alone, Tennessee saw over 1,200 wildfires, making fire protection a top priority for residents.

Get Help With Homeowners Insurance in Tennessee

What your homeowners coverage looks like should be unique to the risks you and your home face. From the protection you need to the discounts you deserve, personalizing your coverage is made easy with Freedom Insurance Group.

We work with several top-rated carriers and help you identify the best coverage for your needs, all available at the lowest price on the market.

Give us a call using the number at the top of the page to speak with a licensed expert who can help you compare your homeowners insurance options in Tennessee easily.

Sources

TDCI. Accessed October 2025.