What Is Personal Liability Coverage?

Summary: Personal liability coverage can help you cover legal expenses and medical bills if a visitor is injured while on your property. Also known as Coverage E, this portion of your home insurance policy can even help you restore a loss to someone else’s personal property if a member of your home causes damage. However, not everything is covered and you’re going to need to adjust your limits according to your risk tolerance. Estimated Read Time: 3 mins

Table of Contents:

- What Personal Liability Coverage Covers?

- What Is Not Covered by Personal Liability Coverage?

- How Much Personal Liability Coverage Do I Need?

- How To Save On Your Coverage E Homeowners Policy in Texas

Also known as Coverage E, your personal liability coverage protects homeowners if there is an injury by a visitor while on their property. Personal liability insurance coverage can also protect you if a member of your home causes accidental damage to someone else’s property.

What Personal Liability Coverage Covers?

With Coverage E, homeowners are covered for expenses such as medical bills, legal fees, or restoring a loss for another party outside of their home. Policy limits exist and are typically set around $100,000, or 50% to 70% of your dwelling coverage. However, this can be adjusted as needed. It’s important to discuss your options with a licensed home insurance agent.

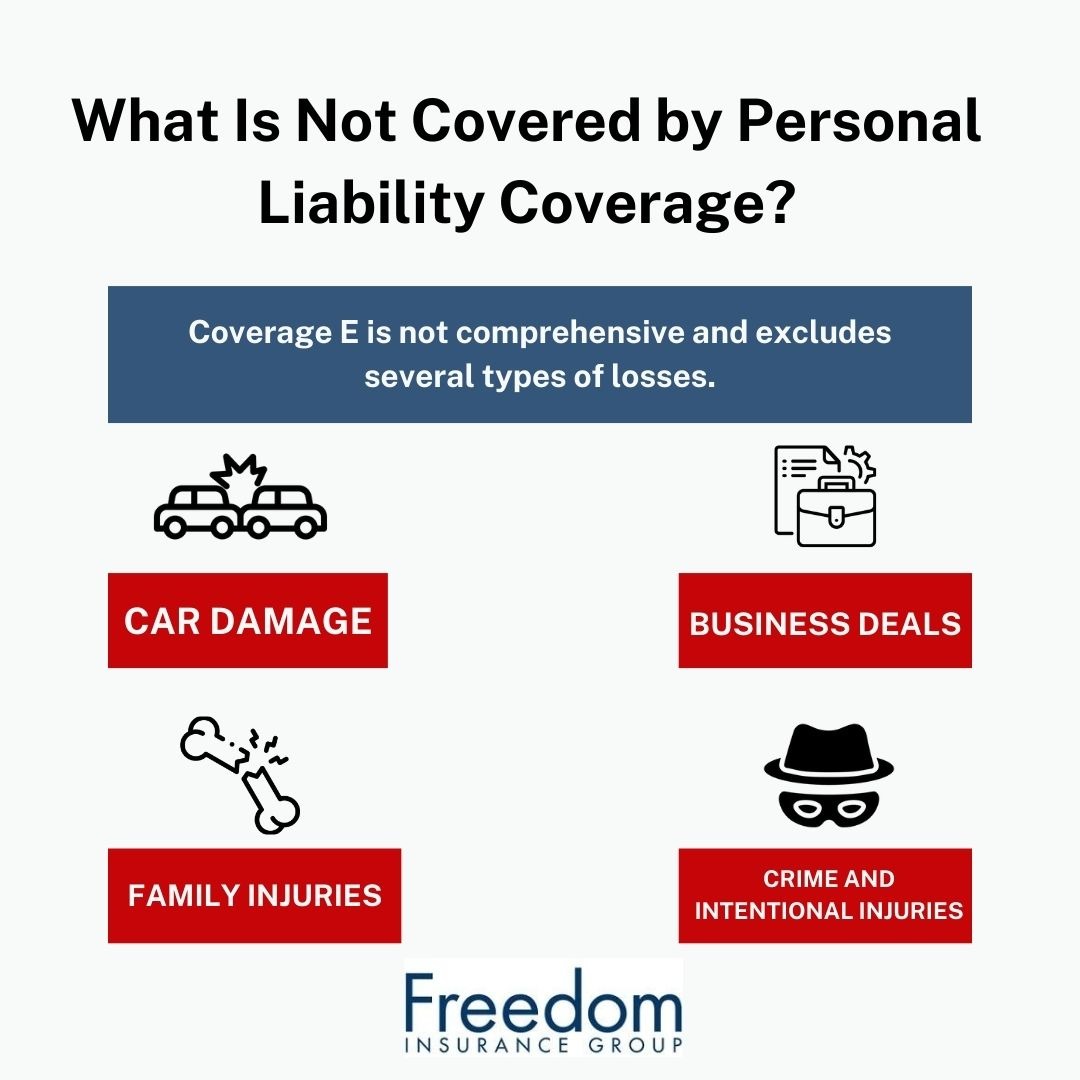

What Is Not Covered by Personal Liability Coverage?

There are many different Coverage E exclusions that either require a different form of insurance or you simply pay out of your own pocket to restore the loss. This includes the following:

- Personal liability involving an automobile isn’t covered. You’ll need to have auto insurance in Texas for such losses.

- Anything dealing with a business will also need commercial coverage.

- Injuries to members of your household aren’t covered, as you’ll need health insurance.

- Finally, if someone is injured by someone on purpose, a member of your household damages someone else’s property intentionally, or a loss occurs while an illegal activity is taking place, the loss is not covered.

Summarizing Coverage

| Category | Covered by Personal Liability | Not Covered by Personal Liability |

|---|---|---|

| Injuries to Guests | Medical expenses for visitors injured on your property. | Injuries to members of your own household. |

| Property Damage | Accidental damage to someone else’s belongings caused by you or family members. | Intentional or criminal damage. |

| Legal Costs | Attorney fees and court costs if you’re sued for covered incidents. | Lawsuits related to your business activities. |

| Pets | Some policies cover injuries or damage caused by pets (check your limits). | Certain breeds or repeated pet incidents may be excluded. |

| Vehicles | You need a separate auto liability insurance policy. | Auto-related injuries or property damage. |

| Business Activities | Requires commercial coverage. | Work-from-home or business-related liability. |

| Coverage Limits | Typically $100,000–$500,000 depending on policy. | Losses above your limit (consider an umbrella policy for extra protection). |

How Much Personal Liability Coverage Do I Need?

The amount of personal liability coverage each homeowner needs varies. Texans should consult with their home insurance agents to determine policy limits and risk tolerance. However, most home insurance policies have between $100,000 and $500,000 worth of coverage. The more personal liability coverage you have, the higher your premiums will be.

How To Save On Your Coverage E Homeowners Policy in Texas

If you want to stay protected for less, there are a few steps you can take. Here’s how to protect your finances from costly liability claims without breaking the bank:

Assess Your Family’s Lifestyle and Risk

You’re going to need to look at your lifestyle and financial risk. This means assessing your assets, the number of people in your household, the activities your household engages in, etc. For example, if you have a lot of financial assets and children who are known to play sports, jump on trampolines, etc., you may need more coverage.

Compare Personal Liability Coverage Insurance Carriers

To save on home insurance in Texas, you need to shop and compare rates. This is why Freedom Insurance Group partners with 25+ home insurance carriers to quickly assess your needs and find the right policy for you. With only a few clicks, you can get a quick, free home insurance quote online. You can also ask an agent about saving on personal liability coverage from trusted Texas carriers.

Sources:

What Is Personal Liability Coverage in Missouri?

Summary: Personal liability coverage (Coverage E) in Missouri protects homeowners if a visitor is injured on their property or if they accidentally damage someone else’s property. This coverage helps with expenses like medical bills, legal fees, and restoring losses to personal belongings, with policy limits typically ranging from $100,000 to $500,000. However, certain exclusions apply, such as auto-related incidents, business activities, injuries to household members, intentional acts, and losses related to illegal activities. The cost of this coverage is included in your home insurance premium, and homeowners can save by assessing their lifestyle, and assets, and by comparing rates. Missourians should work with their insurance agents to determine the right amount of personal liability insurance coverage based on their financial risk and household needs. Estimated Read Time: 3 mins

Personal liability coverage is available for homeowners in Missouri to protect their finances when there are injuries by visitors on their property or in the event a member of their household causes property damage to someone else.

Coverage E is an important part of your home insurance and can be the difference between spending your good hard money on things like legal expenses and medical bills versus moving on with your life.

Below, we’re taking a closer look at how it all works and how to be sure that you have the right level of coverage to avoid surprises.

How Personal Liability Coverage Covers You in Missouri

Personal liability coverage protects homeowners by covering medical bills, legal fees, and property damage caused to others.

You can find policy limits typically starting at $100,000 in Missouri, or 50% to 70% of your dwelling coverage, but this can be adjusted as needed.

Deciding your coverage limits often comes down to risk tolerance and you’re going to need to enroll in a policy that helps you safeguard your finances, for less.

Discuss your risk factors and policy options with a licensed insurance agent to ensure the right protection.

Coverage E Exclusions in MO

Coverage E has several exclusions that require other forms of insurance or out-of-pocket payments.

For example, auto-related liabilities aren’t covered but you can cover these losses through a Missouri auto insurance policy.

Business-related incidents are also excluded and require commercial coverage.

Furthermore, injuries to household members require health insurance and cannot be claimed through your home policy.

Finally, intentional harm to someone, intentionally damaging property, or losses involving illegal activities are not covered.

How Much Is Personal Liability Coverage in Missouri?

The cost of personal liability coverage is included in your home insurance premium, which is affected by many different factors. Here are a few examples:

- Your policy limits.

- The features of your home.

- Your claims history.

- The discounts and bundles you qualify for.

If you want to save on premiums, maintain lower policy limits, enroll in higher deductibles, and bundle your coverage.

Your best way of saving on coverage is to compare policies among various multiple top-rated carriers.

Sacrificing coverage to save a quick buck can leave you paying for expensive losses on your own.

Keep in mind that depending on the level of injury and circumstances, on average, Missouri personal liability settlements can range from over $20,000 to just under $218,000.

Be sure to shop, compare, and save without forfeiting protection that can help you avoid major financial losses due to liability.

Lifestyle and Risk Factors Affect Your Premiums

You’re going to need to look at your lifestyle and financial risk when deciding on coverage, as your policy limits and premiums are going to be affected.

This means when calculating the right level of personal liability insurance coverage on homeowners insurance, you’ll need to assess your assets, the number of people in your household, the activities your household engages in, etc.

For example, if you have a lot of financial assets and children who are known to play sports, jump on trampolines, etc., you may need more coverage than someone with less to lose financially or that engages in fewer risk activities.

Get Personal Liability Coverage Insurance Quotes From Multiple Carriers in Missouri

Saving on Missouri homeowners insurance isn’t always easy, however, if you take the time to compare your coverage needs among multiple carriers, you’ll be able to find the right level of protection at the lowest costs possible.

Our home insurance quote tool below helps homeowners across the Show-Me State compare multiple top-rated carriers.

Get a quote below or ask an agent today about personal liability coverage and how to better protect your household while saving on premiums:

How Much Is Personal Liability Coverage Do You Need in Missouri?

You will find that most home insurance policies provide between $100,000 and $500,000 in coverage for personal liability coverage in Missouri.

When determining the amount of protection that is right for your home, consider the following:

- The higher your policy limits, the higher your premium are going to be. So, be sure you have coverage that works for your budget.

- If you are ok with taking on more risk, having a lower policy limit can help you stay protected and save.

- Umbrella insurance policies are available to help you cover potential losses that go beyond your home insurance policy. This coverage is also known as personal excess liability coverage.

Sources:

What Is Personal Liability Coverage in Tennessee?

Summary: Personal liability coverage (Coverage E) helps homeowners in Tennessee safeguard against financial losses when visitors are injured on their property or if a household member accidentally damages someone else’s property. Starting at $100,000, coverage limits can be tailored to your needs, covering medical bills, legal fees, and lost wages. However, it has multiple exclusions. How much you pay for personal liability coverage insurance depends on your lifestyle, assets, and risk factors, with higher-risk households needing more coverage and paying higher premiums. While comparing policies and using discounts can help reduce premiums, cutting coverage could result in costly out-of-pocket expenses. For extra peace of mind, umbrella insurance is also available. Estimated Read Time: 4 mins

Personal liability coverage is a crucial safeguard for Tennessee homeowners. This portion of your home insurance policy protects your finances when visitors are injured on your property or when a household member accidentally damages someone else’s property.

Also known as Coverage E, the right policy can save you from costly expenses like medical bills or legal fees.

Those financial burdens could fall directly on you without the right policy limits, making a tough situation even harder.

To avoid unpleasant surprises, ensuring you have the right level of coverage is essential.

Let’s dive deeper into how personal liability insurance coverage works and how to make sure you're properly protected.

What Personal Liability Coverage Covers in Tennessee

In Tennessee, personal liability coverage protects homeowners with coverage limits typically starting at $100,000 or 50-70% of your home policy’s dwelling coverage, but can be adjusted to suit individual needs.

Personal liability insurance coverage helps cover medical costs for visitors injured on your property due to negligence and may pay for settlements related to pain and suffering if you're found liable.

Additionally, it covers lost wages from injuries on your property, potential death benefits for accidents, and legal fees.

The coverage also extends to incidents away from home, such as damage caused at a hotel or accidental damage to your neighbor’s property.

Coverage E Exclusions for Tennessee Homeowners

Coverage E comes with plenty of exclusions, including auto-related liabilities, which must be covered by auto insurance in Tennessee, and business-related incidents that require commercial coverage.

Several additional incidents are also excluded from coverage. This includes injuries to household members, which are handled through health insurance, not home insurance.

Borrowed or rented property isn’t covered under many situations, though you may receive coverage depending on the source of the damage and your policy.

Additionally, damage caused during tasks, like damaging your neighbor's property while working or doing a favor, is also not included.

Finally, intentional harm/property damage or losses from illegal activities are excluded.

The Cost of Personal Liability Insurance Coverage in Tennessee

Personal liability coverage is included in your home insurance premium and is influenced by factors such as policy limits, home features, and claims history.

Discounts and bundles can help lower your premiums, and you can save by choosing lower policy limits, higher deductibles, or bundling your coverage.

Comparing policies from top-rated carriers is essential for reducing costs, but be cautious—reducing coverage to save money could lead to expensive out-of-pocket losses.

The average cost of personal liability settlements in Tennessee is nearly $456,000, so it's important to find adequate coverage to protect from this costly risk.

Remember, you can shop multiple carriers to save on premiums without giving up protection against potentially large financial losses.

Factors That Affect How Much You Pay

The cost of Coverage E on your homeowners policy is affected by your lifestyle and financial risk.

Policy limits and premiums are also influenced by your assets, household size, and daily activities.

If your household engages in higher-risk activities, like kids playing sports or using swimming pools, you may need more coverage.

On the other hand, if you have fewer financial assets or engage in less risky activities, you might opt for lower coverage.

Tailoring personal liability insurance coverage on homeowners insurance to meet your unique needs is the key to finding the right protection and saving money on your premiums.

Get Quotes From Tennessee Carriers to Save

Saving on Tennessee homeowners insurance can be challenging, but comparing coverage needs across multiple carriers can help you find the best protection at the lowest cost.

It’s important to review your policy for potential ways to save as well as outdated policy limits that may not fit your current lifestyle.

Remember, your personal liability coverage should be enough to keep your family from having to endure a major financial loss after the loss of another party.

Use our home insurance quote tool below to compare top-rated carriers in the Volunteer State or ask an agent how we can help you save on your coverage.

How Much Is Personal Liability Coverage Do You Need in Tennessee?

Most home insurance policies in Tennessee offer between $100,000 and $500,000 in personal liability coverage, with higher limits leading to higher premiums.

If you're comfortable with a bit more risk, opting for lower limits can help you save.

For added peace of mind, umbrella insurance—also known as personal excess liability coverage—can extend your protection beyond your standard policy.

It's a smart option to safeguard against larger, unexpected losses.