The Best Home Insurance Rate and Shopping Guide in Texas

Summary: Throughout the Lone Star State, you’ll find a diversity unlike any other. From robust metros such as Dallas, Houston, and Austin to the Gulf Coast region and even rustic regions in Central Texas, the state has a lot to offer. Discover homeowners insurance in Texas that meets your specific needs no matter where you call home. Estimated Read Time: 8 mins

Table of Contents:

- How Much Is Home Insurance in Texas?

- What Does Homeowners Insurance Cover in Texas?

- Why Is Home Insurance So Expensive in Texas?

- Do You Have To Have Homeowners Insurance in Texas?

- Pros and Cons of Homeowners Insurance

- How to Shop for Homeowners Insurance in Texas

- Homeowners Insurance Quotes in Texas

How Much Is Home Insurance in Texas?

Homeowners insurance in Texas is among some of the highest in the United States. The average home insurance cost will run you $2,255 per year or around $188 per month. A figure that can change dramatically depending on a host of individual and statewide factors.

One of the reasons the Lone Star State has such high home insurance rates is because there are a wide variety of perils that could damage your home From the Gulf Coast cities protecting against hurricanes to Hill Country protecting against hail and even North Texas protecting against tornadoes. There are a lot of unique perils that could damage your home.

The more likely it is for your home to suffer a loss, the higher your premiums will be. Riskier homeowners pay more on average. Therefore, to get the best home insurance, do what you can to mitigate your risk of loss.

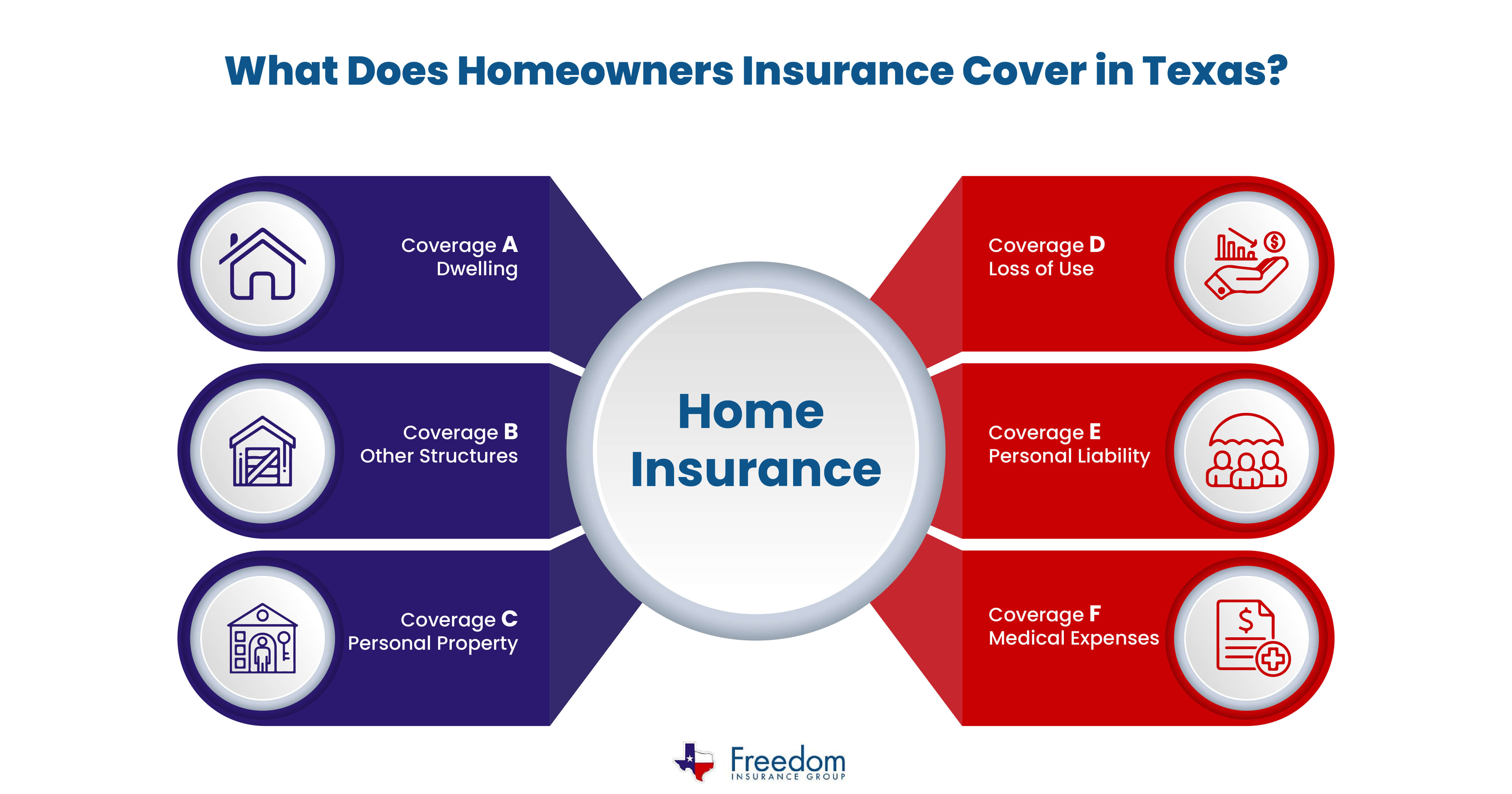

What Does Homeowners Insurance Cover in Texas?

Your homeowners insurance policy is actually a collection of many different coverages. This allows you to not only protect your home but other property you own and even yourself from liability. In other words, Texans are provided a wider breadth of protection at an affordable rate. Here’s how a standard home insurance policy (HO-3) breaks down its protections:

Your homeowners insurance policy is actually a collection of many different coverages. This allows you to not only protect your home but other property you own and even yourself from liability. In other words, Texans are provided a wider breadth of protection at an affordable rate. Here’s how a standard home insurance policy (HO-3) breaks down its protections:

Coverage A - Dwelling

The balk of your coverage comes from your policy’s dwelling coverage. Here, you’ll find protection against open perils that may affect your home’s physical structure and attached structures. Some examples include the following:

- Hail damage that damages your roof.

- A kitchen fire that destroys your appliances, counters, cabinets, walls, etc.

- Wind damage that causes significant damage to your siding and attached garage.

Coverage B - Other Structures

Home insurance will also protect the other structures on your property including fences, detached garages, sheds, and mailboxes. Just as your home is protected, your policy covering additional structures can help you restore expensive losses through affordable protection. A typical policy will cover a loss of up to 10% of your home’s value.

Coverage C - Personal Property

Your personal possessions including electronics, clothing, furniture, etc. are also protected against named perils. Personal property coverage comes with policy limits, so for more expensive valuables, you may need to purchase additional coverage options. However, most homeowners insurance policies range between 25%-50% of your home’s dwelling coverage limit.

Coverage D - Loss of Use

In the event you were to suffer a loss in which your home is unlivable in the aftermath, your home insurance policy is there for you with loss of use coverage. It’ll cover living expenses such as hotel rooms and dining until you are capable of getting back on your feet. Most HO-3 policies will cover 20% of your home’s insured value for loss of use claims.

Coverage E - Personal Liability

If someone is visiting your property and becomes injured, as a homeowner, unfortunately, you can be held liable. Your homeowners insurance policy provides specific protection to help mitigate medical and legal expenses related to such incidents. Your policy’s personal liability limits depend on a variety of factors but homeowners are encouraged to maintain a minimum of at least $100,000 in coverage.

Coverage F - Medical Expenses

Visitors who are injured while visiting your property can find homeowners liable for damages. Should someone become injured, your homeowners insurance policy will help pay for medical expenses with Coverage F to avoid having to pay for these expenses on your own. It is important to note that this coverage does not include members of your household. For medical expenses involving members who reside in your home, you’ll need the proper health insurance policies or pay the expenses on your own. Medical expenses covered by your home insurance are typically limited to around $2,000-$5,000 worth of coverage.

Additional Home Insurance Coverages in Texas

In addition to the standard coverages your policy provides, there are endorsements, or riders, that protect you from additional perils. For example, if you have expensive collectibles that exceed your homeowners policy’s coverage limits, scheduled personal property coverage is available for extra protection.

There are several additional examples. Some riders may protect against sump pumps and sewage backup, while other endorsements can protect against things such as a damaged utility line. Your coverage needs are unique and enrolling in personalized coverage will help you avoid expensive losses

Why Is Home Insurance So Expensive in Texas?

There are several reasons the cost of homeowners insurance continues to rise for Texans. Not only do individual factors come into play but also regional and statewide trends. These are some common examples of perils your home may face:

- Severe thunderstorms/windstorms

- Hail damage

- Wildfires

- Tropical storms/hurricanes

- Flooding

- Theft

- Water damage and freezing

It doesn’t matter where you look, there is severe weather found throughout the Lone Star State. Costly labor and materials that keep going higher mean expensive claims require higher premiums as businesses maintain revenue and profits.

But it’s also important to note that the risks you pose as a client are also looked at by each carrier differently. This means that if you are looked at ask a high risk by by some companies, you may not be by others. Always shop around to determine the lowest cost for home insurance.

Do You Have To Have Homeowners Insurance in Texas?

You aren’t required by law to have homeowners insurance in Texas, however, failing to do so means you’ll need to cover any losses on your own. But it goes deeper than just fixing damage to your home, as you’ll need to cover the eating and lodging expenses if your home is uninhabitable after a loss, potential lawsuits due to liability, and any losses to other pieces of property otherwise covered.

It’s also worth noting that while the law may not force you to have a policy, your mortgage might. Virtually any mortgage that you use to finance the purchase of your home is going to have to maintain a valid home insurance policy as a term and condition of the loan.

Pros and Cons of Homeowners Insurance

It’s always recommended to maintain homeowners insurance in Texas. Doing so will protect your home and more but there are pros and cons to having a policy. Ultimately, the decision is up to you, but so too is the risk of forgoing coverage. Here’s a closer look at both sides:

|

Pros: |

Cons: |

|

You’re protected against potential losses that would otherwise be unaffordable |

Costs can be quite high if you fail to shop around and find coverage |

|

Peace of mind knowing that you can restore your home if something were to go wrong |

Even with affordable coverage, many homeowners may feel as if it’s a waste of money if they never submit claims |

|

You’ll be able to maintain shelter if your home is not livable after a major loss |

Your coverage is not comprehensive and many scenarios may require additional protection |

|

Homeowners protect more than just their homes, including their assets and additional property |

Understanding your policy may be difficult and if you aren’t careful the terms and conditions of your policy may create confusion |

How to Shop for Homeowners Insurance in Texas

To find the best homeowners insurance for your home, you’re going to need to shop around, but how you go about things is going to affect your journey. Thankfully, there are simple steps to remember that won’t only help you find the right coverage but also save money in the process. Here’s how you do it:

Identify Your Home’s Potential Perils

Your first step is to identify what perils your home is facing. There are some baseline perils, such as fires and theft, that are universal. However, some homes may require additional coverage or considerations to protect against. Working with a licensed insurance agent can help you review potential losses your home may be at risk for and the right coverages to protect against them.

Shop and Compare From Many Different Carriers

Remember, everyone is going to have different personal factors that can affect premiums, but it’s also worth noting each carrier assesses these factors differently. What may be a major risk for one brand may not be as big of a deal for another. Therefore, you’ll need to shop and compare your options you may end up overpaying for the same protection. Comparing carriers, coverages, and discounts is the best way to save money as a homeowner.

Work With a Professional Home Insurance Agent

The benefit of working with an insurance agent is that not only is the process quicker, but you’re also getting an expert to help guide you. Insurance brokerages work with a variety of partners to provide multiple brands to homeowners and agents can help you search through the carriers in your area that best fit your needs for the lowest price.

Homeowners Insurance Quotes in Texas

Getting a homeowners insurance quote is a fast, easy way to check premiums in your area. Since 2005, Freedom Insurance Group has been making it easy for homeowners in Texas to save on coverage and protect their homes from potential perils.

Our team is available to help you find the coverage you need at the lowest price available. On average, people who switch save 40% on their premiums each year. Get a free homeowners insurance quote and see how much we can help you save today!