Affordable Landlord Insurance in Texas

How Much is Landlord Insurance in Texas?

The short answer: Typically about 15-25% less than standard homeowners insurance, with annual premiums ranging from $1,300 to $4,600 or higher, depending on the property type, location, value, and specific risks. For a standard single-family rental, expect averages between $1,800 and $3,000 per year. Coastal spots like Houston face steeper costs due to hurricane threats, while hail-prone areas around Dallas-Fort Worth can also drive up rates. With climate risks intensifying and construction costs rising due to inflation, premiums have climbed about 8% on average heading into 2026, making shopping around more crucial than ever.

Why?

Insurance brands all assess the same thing when taking you on as a client: the amount of risk you pose. If you have more risk, you’ll find that you’ll pay higher premiums, whereas if you pose less risk to a company, your premiums will be lower. Rental properties are assessed across the insurance industry as properties that come with more risk.

There are many reasons for this including the fact that the policyholder isn’t present. Each home is different as there are different factors surrounding each property including the home’s age, location, condition, and more. This means that no two premiums will be the same and rates will differ from property to property. At Freedom Insurance Group, we help landlords save an average of 40% on their premiums each year and have various affordable low-cost options.

Around 38% of all homes in Texas are renter-occupied. This is a considerable figure for the second-largest state in America in terms of both land size and population. Landlords have plenty of responsibilities and properties to handle in the Lone Star State and a landlord insurance policy is the first step.

If you are a landlord, you understand firsthand the risks that come with your investment. There are all of the normal perils which can affect your own home coupled with the fact that you are entrusting another party to maintain your property as you would. Combined with the legal obligations landlords have to take care of their tenants and things can add up quickly.

Fortunately, landlord insurance in Texas is affordable protection that can help you maintain peace of mind and prepare for what may come. From losses involving property to liability concerns and more, your landlord policy mitigates losses you might face and will help you restore your rental property should a hazard strike.

What Landlord Insurance Covers

A landlord insurance policy is also called a dwelling fire policy. Similar to a traditional home insurance policy, your landlord insurance will provide coverage that protects your home’s structure, and other structures on your property, and against some liability, but in its own unique way. Let’s explore how your landlord insurance protects you:

- Dwelling Coverage- Your rental home’s dwelling, including attached areas such as garages, is protected against a number of perils including fires, wind/hail damage, vandalism, and more. This includes apartments and condos.

- Other Structures Coverage- The other structures on your rental property, such as a fence or detached garage, are covered by the perils listed in your policy.

- Personal Property Coverage- Your personal property is covered by your landlord insurance policy, so long as the personal property affected is critical to maintaining the property. Your tenant’s property is not covered by your landlord insurance policy. An example would be a fire that destroys your washer and dryer as well as your tenant’s clothing. You can file a claim for your home and appliances, but your tenant’s clothing would require a renters insurance policy on their end to file a claim for the loss.

- Loss-of-Income Coverage- If your property becomes uninhabitable and loss-of-rental income were to take place because of it, you may file a claim with your landlord insurance. When tenants refuse to pay, you may be covered by your standard landlord policy, but you may also need additional coverage to file a claim. Each policy is different and reading the terms and conditions of your individual policy is your best course of action. Speaking with an insurance agent is also highly recommended.

- Liability Coverage- If there is an injury that occurs on your rental property and you are found responsible for it, you may face paying for expensive medical and legal fees. Your landlord insurance policy provides protection to mitigate such exposure and will help you pay for these expenses to avoid a financial loss out-of-pocket.

The following are common perils your landlord insurance will protect you from:

- Fire, lightning, and smoke damage.

- Wind and hail damage.

- Riots and civil commotion.

- Explosions.

- Damage from aircraft and vehicles.

- Sudden and accidental water damage (does not include flooding).

- Volcanic eruptions.

- Vandalism.

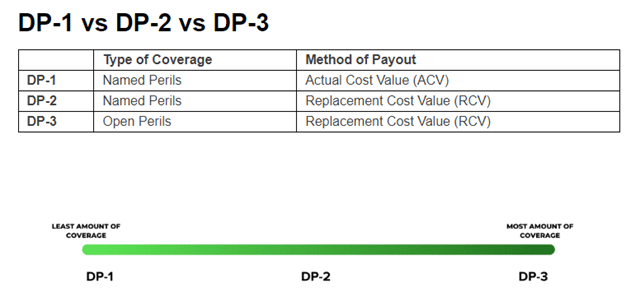

There are three different dwelling property insurance types landlords may use to protect a rental property. The more extensive your coverage, the more your property will be protected from:

| Insurance Policy | Description |

| DP1 | A DP1 policy is the most basic form of dwelling fire coverage. Your policy will protect against named perils, meaning if the peril is named on your policy, you are covered. |

| DP2 | Offering more coverage than a DP1 policy, you’ll also operate under a named peril basis, but there are more perils you are protected from. This includes burglary damage, the weight of snow and ice, electrical damage, accidental overflow of water and steam, frozen pipes, falling objects, loss of rent, and more. The specifics of your policy may differ by insurance provider and because you are protecting against more, DP2 policyholders will pay a bit more in premium. |

| DP3 | The most common form of dwelling fire coverage. Here, landlords gain the best form of protection and a policy that is an open peril-based coverage. Your DP3 policy most resembles a home insurance policy and is the recommended form of protection from insurance experts including Freedom Insurance Group. |

What’s important to remember about your landlord insurance policy is that it is not blanket coverage, but it does protect you from a variety of losses.

Every landlord owes it to themselves and their tenants to prepare for potential losses through insurance policies built to protect against property loss, personal liability, and a loss of income.

Common Exclusions to Your Landlord Coverage

Again, landlord coverage won’t cover everything. Here are some of the biggest misconceptions that are not covered by your policy:

- Flood damage.

- Intentional damage from a tenant.

- Your tenant’s personal belongings.

- Earth movements.

- War.

- Mold damage.

- Government action, local ordinances, and laws.

- Nuclear hazards.

Shared property (landlord insurance is reserved for a non-owner-occupied property).

Additional Coverages Beyond a Dwelling Fire Policy

Because exclusions to your policy exist, you may find yourself facing perils that require additional forms of protection. Thankfully, landlords have options available to mitigate other potential losses. Consider these coverage options that will protect you and your investment by picking up where your landlord insurance policy lets off:

- Flood Insurance- Flood events are not covered by landlord insurance and you’ll need a separate policy.

- Vandalism Coverage- Not all landlord policies come with vandalism coverage, and if it is not included in your policy, you may want to consider either upgrading your coverage or purchasing additional protection.

- Building Code/ Construction Coverage- When damages occur, you may be forced to upgrade your rental property to remain in compliance with new building codes. This coverage helps offset those construction costs to keep you in line with the law without hurting your own pockets to do so.

You can also purchase loss-of-income coverage if your dwelling fire policy does not protect against such perils.

Why You Need Landlord Insurance

While you don’t have to have a landlord insurance policy in Texas by law, failing to have the right coverage can cost you dearly. When you consider the amount of money it would take to repair serious damage, rebuild your rental home, cover medical and legal costs, or overcome the loss of rental income, affordable landlord coverage just makes sense. A major fire or a visitor slipping and falling on a damaged staircase can turn your rental property from a sound investment into an unescapable money pit.

The Top Cities in Texas in Need of Landlord Insurance

With over 4.2 million homes rented in the state, plenty of landlords can benefit from landlord insurance no matter where you look in Texas. Still, some cities have more rentals than others. These are some of the top cities in Texas featuring rental properties in need of protection from a landlord insurance policy:

- College Station, Texas

- San Marcos, Texas

- Humble, Texas

- Killeen, Texas

- Dallas, Texas

- Houston, Texas

- Austin, Texas

- Lewisville, Texas

- Bryan, Texas

- Waco, Texas

How to Save on Landlord Insurance

The best way to save on your landlord insurance is to take advantage of bundling your policy with another. If you have multiple properties in need of protection, you can enjoy a multi-policy discount, or you can combine your home and/or auto insurance with your landlord policy. These are a few other discounts available to landlords that can help you lower your costs:

- Claims Free Discounts- If you haven’t submitted a claim within a certain period of time, your insurance provider may offer you a discount at renewal. Terms may vary, but some brands require a 5-year claim-free period.

- Comparing Your Coverage- Landlords save more when shopping among a variety of insurance brands to find the lowest price for their needs.

Get a Free Instant Landlord Insurance Quote

By working with over 25 top-rated insurance brands, the team at Freedom Insurance Group can comparison shop your coverage to locate the lowest rate on the market for your protection. Contact us today to take the hassle out of finding an insurance policy for your rental properties, or, enjoy a free online landlord insurance quote.

FAQs About Landlord Insurance in Texas

Being a landlord has a variety of unique challenges and you are bound to have questions. Our team of experts is here to answer any landlord insurance-related questions, however, some come up more than others. Feel free to contact us at any time for your insurance needs, or, refer to these frequently asked questions (FAQs) to learn more.

Is Tenant Damage Covered by My Landlord Insurance Policy?

Accidental damage caused by a tenant is covered by your landlord insurance policy in Texas. If a tenant intentionally damages your home, however, your policy does not always cover it. This coverage can sometimes be added by a special endorsement. Landlords dealing with intentional damage from tenants will have to seek damages through pursuing legal options, including filing against the tenant’s renters insurance coverage.

Will a Homeowners Insurance Policy Cover My Rental Home?

No, you’ll need landlord insurance, also known as a dwelling fire policy, to protect your rental. A homeowners insurance policy will not protect a home uninhabited by the policyholder.

Does Landlord Insurance Cover Flood Damage?

No, for flood damage to your rental to be covered, you’ll need a flood insurance policy. Water damage may be covered by your landlord insurance policy if it is of a sudden and accidental nature, but not for general wear and tear or slow leaks.

Do I Need Landlord Insurance for My Airbnb Property?

For short-term rentals and home-sharing such as Airbnb, most hosting sites will offer their own insurance policies. Of course, these protections can often be complicated to file and might not be enough to cover damages.

A landlord insurance policy nor a home insurance policy are likely to help for short-term rentals as your insurance provider will likely see your rental operations as a business.

The best course of action is to contact your insurance provider before renting your home through Airbnb or a similar service to determine the best course of action. Failure to disclose such information can result in you being dropped as a client and a lapse in coverage for your home.

Can I File a Claim if My Rental Home is Vacant at the Time?

Different policies will have different limitations, but filing a claim with a vacant property can make things more difficult. The best option you have as a landlord is to maintain a resident at your property and to speak with your insurance agent about the specifics of your policy.

{kind=link}