Compare Umbrella vs. Excess Liability Insurance in Texas

Summary: Umbrella and excess liability insurance both provide extra protection beyond standard policies, but they differ in coverage scope. Umbrella insurance offers broader protection, covering various liability risks, while excess liability extends existing policy limits without adding new coverage types. Texans should consider these options to safeguard assets against costly lawsuits, medical expenses, or property damage. Comparing policies ensures adequate protection for high-value homes, vehicles, and other assets against financial losses. Estimated Read Time: 4 mins

Excess liability and umbrella insurance, while similar, are different forms of protection. Homeowners in Texas need to understand the difference if they are to protect against potential losses properly. Comparing umbrella insurance vs. excess liability can help homeowners save thousands of dollars when facing a major loss due to liability.

What’s the Difference Between Umbrella vs. Excess Liability Insurance?

The comparison of Texas umbrella insurance vs. excess liability is important because despite working in similar ways, they have different protections.

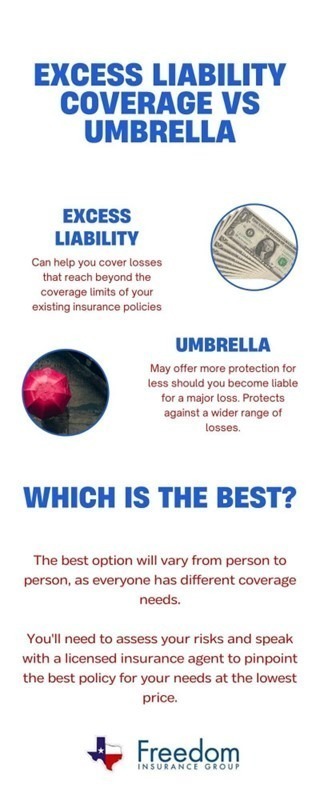

Simply put, the best coverage between excess liability and umbrella insurance will vary from person to person, however, they both aim to protect against larger losses where your personal assets may be at risk:

Umbrella Coverage

Often confused as umbrella excess liability insurance, an umbrella policy provides you with a wide range of liability protection when such losses exceed the liability found in a home or auto insurance policy. Umbrella insurance can often provide a great amount of protection for a lower cost.

Excess Liability Coverage

Also known as excess umbrella liability insurance, your coverage picks up where your liability coverage stops. This is in case you are facing a loss that is beyond your policy limits but must be accompanied by another insurance policy, whose protection comes first.

Why Texans Should Consider Excess Liability vs. Umbrella Insurance

Having the right coverage is imperative as both the cost of medical expenses and restoring property damage also continue to rise.

America is home to one of the most expensive healthcare systems on the planet and the cost of labor and repair for physical damage, are also rising.

Liability can come in many forms but if you are found liable for either loss involving bodily injury or property damage to another party, you’ll need to find a way to restore these losses.

Failing to have adequate coverage can cost you in a variety of ways, including these common, everyday scenarios:

- You’re a homeowner and someone is injured while visiting your home.

- You host gatherings at your home, especially with high-risk features such as a swimming pool.

- You routinely have help at your home such as a housekeeping service or landscaping service.

- You have children, especially those of driving age.

- You have several high-valued assets including things such as a boat, luxury vehicle, or luxury home.

- You’re accused of libel on the Internet.

- You cause a car accident where the damages exceed your auto insurance coverage.

Furthermore, the U.S. legal system is ranked as the most expensive in the world, and facing such financial downfalls in the midst of trying to pay to restore a loss can be detrimental to your finances and assets, including your home.

Choosing between umbrella insurance vs. excess liability comes down to providing your household with enough protection to keep you financially stable.

How to Protect High-Valued Properties With Umbrella vs. Excess Liability in Texas

There are three common risks homeowners may face that could cause them to be liable for another party’s loss:

- Someone injures themselves while visiting your home.

- You’re involved in a car accident in which losses beyond your auto policy’s limits occur.

- You or someone in your household is responsible for the injury or destruction of property to another party.

Particularly for those with high-valued homes, having the right coverage in place is essential, as the affected party could target your house and personal property.

For example, let’s say you have a home worth $700,000, an investment portfolio worth another $500,000, luxury vehicles worth $200,000, and watercraft totaling $100,000.

If you are found liable for someone’s loss and it’s severe enough to reach, for example, $2.5 million, but you only have $1 million in coverage, those assets are now on the line.

Never mind the fact that you will also have legal expenses to pay in many cases, you could lose your home, your investments, your vehicles, and more.

The bottom line is that just because you have coverage doesn’t mean you have enough and just because a loss is so severe it surpasses whatever coverage you do have, it doesn’t mean it goes away.

Comparing umbrella and excess liability insurance helps you avoid losing your assets, money, and time after an excessive loss.

Compare Quotes for Umbrella vs. Excess Liability in Texas

Texans have enough to worry about, excessive liability claims shouldn’t be one of them.

Protect yourself with the right coverage and compare top-rated insurance carriers near you to find the lowest possible price.

Contact us at (972)798-3769 to ask an agent to compare umbrella vs. excess liability insurance quotes today.