How Does My Mortgage Escrow Pay My Home Insurance?

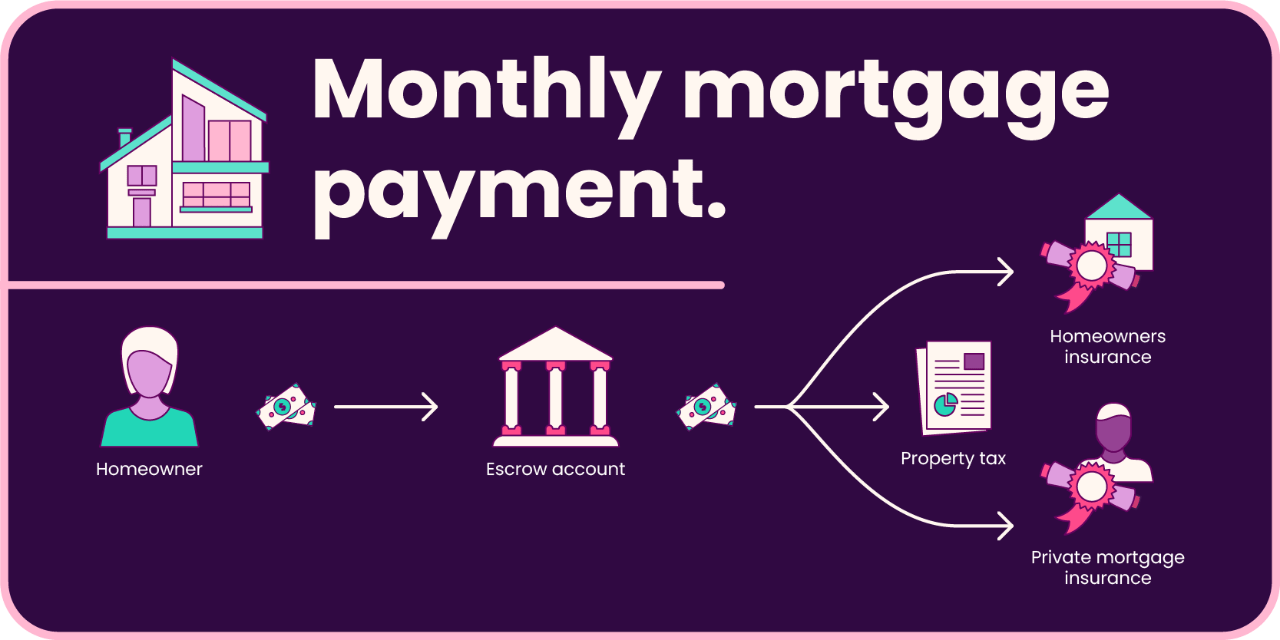

When you have a mortgage, your lender might require you to set up an escrow account to ensure that property taxes and homeowner’s insurance are paid on time. Here’s how the process typically works:

- Setting Up the Escrow Account:

- When you close on your home, your lender will often set up an escrow account for you.

- Monthly Payments:

- Along with your monthly mortgage principal and interest payment, you’ll also pay a portion of your annual property taxes and homeowner’s insurance.

- This portion is typically one-twelfth of the annual total (though it can vary based on when taxes/insurance are due and the specifics of your escrow agreement).

- This monthly amount gets deposited into your escrow account.

- Payment of Taxes and Insurance:

- When your property taxes and homeowner’s insurance bills are due, your lender uses the funds in the escrow account to pay them on your behalf.

- This ensures that these critical bills are paid on time, protecting both you and the lender’s investment in the property.

- Annual Escrow Analysis:

- Lenders typically perform an annual escrow analysis to make sure that the amount being collected each month will cover tax and insurance bills.

- If the bills were higher than expected and your escrow account has a shortage, you might be asked to pay a lump sum to cover it. Alternatively, your monthly escrow contribution could be increased.

- If the bills were lower than anticipated, leading to an overage in your escrow account, the lender might refund the overage or adjust your monthly payments downward.

- Changes in Insurance or Taxes:

- If your property taxes or homeowner’s insurance premiums change (which they often do), your monthly escrow payment will likely change too.

- If you’re notified of a change in your insurance premium, it’s a good idea to notify your lender to ensure they adjust the escrow amounts appropriately.

- Changing Lenders or Refinancing:

- If you refinance or change lenders, you will have to set up a new escrow account. Any funds in your old escrow account will be refunded to you.

- It’s essential to ensure that bills are not accidentally paid twice during the transition.

Remember that while escrow accounts offer convenience and ensure timely payment of taxes and insurance, they also mean you need to trust your lender to handle these payments correctly. Always keep an eye on your escrow statements and any tax or insurance bills you receive to ensure everything is being paid as it should be.