Types of Texas Home Insurance Policies and Coverages

Different types of Texas homeowners need different types of home insurance. Whether you’re a single-family homeowner, condo owner, mobile homeowner, or renter, there’s an insurance policy designed to protect what you own.

We’ll explain what each home insurance policy type covers and how to make sure you get the coverage you need with this Ultimate Guide:

- HO-1: Basic form

- HO-2: Broad form (structure covered for broad/named perils)

- HO-3: Special form (structure covered for special/open perils)

To learn more about Broad/Named Perils vs Special/Open Perils coverages click “Texas Open Perils versus Named Perils Explanation”

- HO-4: Contents broad form

- HO-5: Comprehensive form

- HO-6: Unit-owners form

- HO-7: Mobile home form

- HO-8: Modified coverage form

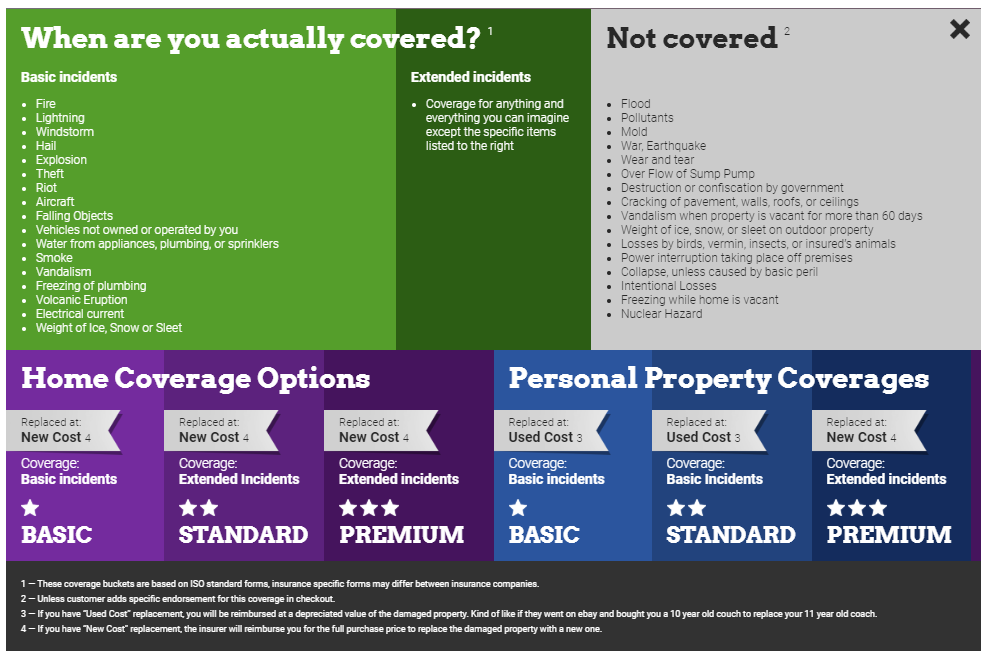

Homeowners policies combine several types of coverages into one policy. Most homeowners policies in Texas include these basic six coverages for property and liability. However, what they are covered for and their exclusions by the type of form chosen ie HO-1, HO-3, etc. The form types are further below.

- Dwelling coverage pays if your house is damaged or destroyed by something your policy covers.

- Personal property coverage pays if your furniture, clothing, and other things you own are stolen, damaged, or destroyed.

- Other structures coverage pays to repair structures on your property that aren’t attached to your house. This includes detached garages, storage sheds, and fences.

- Loss of use coverage pays your additional living expenses if you have to move while your house is being repaired. Additional living expenses include rent, food, and other costs you wouldn’t have if you were still in your home.

- Personal liability coverage pays medical bills, lost wages, and other costs for people that you’re legally responsible for injuring. It also pays if you’re responsible for damaging someone else’s property. It also pays your court costs if you’re sued because of an accident.

- Medical payments coverage pays the medical bills of people hurt on your property. It also pays for some injuries that happen away from your home – if your dog bites someone at the park, for instance.

| Policy Form | Property Type | What It Covers | Best For |

| HO-1 (basic) | House | Limited named perils for structure and contents | Bare-bones coverage, where available |

| HO-2 (broad) | House | Greater number of named perils for structure and contents | More coverage than HO-1 but less than HO-3 |

| HO-3 (special) | House | Open perils for structure, named perils for contents | Most homeowners |

| HO-4 (contents broad) | Rental unit | Named perils for contents | Renters |

| HO-5 (comprehensive) | Higher-value house | Open perils for structure and personal property | Homeowners who want the most comprehensive coverage |

| HO-6 (unit-owners) | Condo or co-op unit | Named perils for contents and certain structural items | Condo or co-op unit owners |

| HO-7 (mobile home) | Mobile home | Open perils for structure, named perils for personal property | Mobile home owners |

| HO-8 (modified coverage) | Old, high-risk homes | Limited named perils for structure and personal property | Homeowners who don’t qualify for any other coverage |

What each form covers can vary by insurance company and state (including Texas)

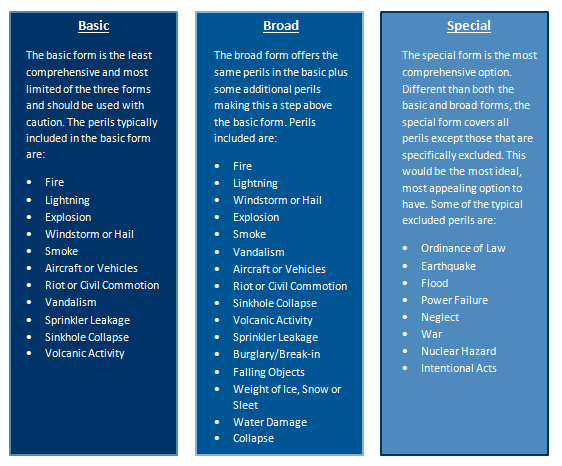

HO-1: Texas Basic form

Best for: Bare-bones coverage, where available

This basic homeowners insurance policy only covers losses caused by a peril named in the policy. The most common perils covered by an HO-1 policy include:

- Fire or lightning

- Smoke

- Windstorms or hail

- Explosion

- Aircraft

- Vehicles

- Vandalism

- Theft

Few homeowners have this type of policy. An exception is Texas, where it’s called an HO-A policy and provides coverage to homeowners who can’t otherwise get it.

Good to know: In designated catastrophe areas with a history of major hurricane losses, homeowners don’t get windstorm or hurricane coverage under this policy and must purchase it separately.

HO-2: Texas Broad form

Best for: TX Homeowners who can’t afford an HO-3 policy

Homeowners who want more coverage than an HO-1 policy offers might choose an HO-2 policy. You might also opt for an HO-2 policy if you can’t afford a more comprehensive HO-3 policy, or if no insurers in your area offer HO-3 policies.

Like the HO-1, the HO-2 form is a named perils policy for your structures and belongings. However, it protects against a greater number of named perils than an HO-1 policy. In addition to the perils covered by an HO-1 policy, an HO-2 policy generally includes coverage for:

- Falling objects

- Weight of ice, sleet, or snow

- Freezing pipes

- Sudden and accidental water discharge.

HO-3: Texas Special form

Best for: Most Texas homeowners

The HO-3 policy is the most common type of homeowners insurance policy. For your home and other structures, it’s an open-perils policy, meaning it covers any damages unless the cause of damage is explicitly excluded by the policy.

Here’s what’s generally not covered under an HO-3 policy:

- Earthquake

- Flood

- Wood-destroying insects

- Vermin

- Wear and tear

- Lack of maintenance or neglect

- Intentional damage

- Wind or hail damage to trees

- Vacant property

- Continuous water leakage or seepage

- Sewer backup

- Acts of war

- Mold (depending on the cause)

Personal property is still covered on a named-peril basis.

HO-4: Texas Contents broad form

Best for: Texas Renters

If you’re a renter, you don’t need coverage for the structure you live in; that’s the owner’s responsibility. However, the owner’s home insurance policy won’t cover your personal belongings, nor will it provide liability protection if someone gets hurt in your unit and sues you. That’s why you need renters insurance. HO-4 policies cover the same named perils that HO-3 policies cover.

HO-5: Texas Comprehensive form

Best for: TX Homeowners who want to maximize their coverage

If an HO-3 policy doesn’t provide enough coverage for you, an HO-5 policy may be what you need. This type of policy provides open-perils coverage for both the structure and your personal property. It’s more popular than HO-2 or HO-1 coverage, but far less popular than HO-3 coverage.

HO-6: TX Unit-owners form

Best for: Texas Condo and co-op unit owners

When you own a unit in a condominium or co-op building, the condo association will carry a master insurance policy that covers the building’s exterior and common areas. However, the building policy won’t cover the improvements to your unit or your personal possessions, nor will it offer you personal liability coverage.

When you’re buying an HO-6 policy, or condo insurance, you’ll first need to learn exactly what your building’s master policy covers. Then, you’ll want to find a unit-owners policy that picks up where that coverage leaves off.

Pay close attention to coverage for special assessments. It can be a major asset if the building experiences covered losses beyond what its insurance and reserve funds can pay for. When the association asks its members to help cover the shortfall, you can turn to your policy instead of your savings account.

HO-7: Texas Mobile home form

Best for: TX Mobile home owners

If you own a mobile home, you’ll want this insurance for your dwelling and personal property. It provides similar coverage to an HO-3 policy.

An HO-7 policy may not automatically cover your home while it’s in transit, however, so if you anticipate a move, check to see if you’ll need supplemental coverage.

HO-8: TX Modified coverage form

Best for: Texas Owners of old homes

HO-8 policies provide very limited coverage, similar to an HO-1 policy, but are even less popular. You’re most likely to encounter this policy in Oklahoma, Mississippi, and Arkansas.

HO-8 policies are designed to insure homes that would cost much more to replace than they’re currently worth. For example, think of a home built in the 1880s with materials and features that aren’t common today — and the home is in a neighborhood that’s no longer popular, so its value is depressed.

In addition, an HO-8 policy may be the only option available for homes that don’t meet insurers’ risk requirements for other policy forms.

Additional insurance policy options

No matter which of the above forms your policy is based on, you might want supplemental coverage for certain situations. These are some common options:

- Texas DP-1 insurance: This limited policy covers basic named perils only and provides actual cash value rather than replacement cost coverage. It’s intended for vacant properties or standalone structures, but all occupancy types are eligible for coverage. It doesn’t provide liability or personal property coverage unless you add these features.

- Texas DP-3 insurance: This policy is also known as a landlord’s policy as it covers rental properties. A DP-3 policy covers the building’s structure, provides liability coverage for accidents, and protects your rental income if your tenants have to move out due to a covered loss.

- Personal umbrella policy: This insurance provides additional liability coverage above the limits of your standard homeowners insurance policy. You’ll need to carry a higher level of underlying coverage to be eligible. It can be indispensable if someone is seriously injured on your property and has damages of $1 million or more.

- Scheduled personal property coverage: If you own any high-value personal possessions, you’ll need to purchase scheduled coverage to fully insure them. The personal property coverage under your dwelling policy limits how much it pays out for expensive items, such as jewelry and electronics.

- Water backup coverage: If your sump pump fails or a drain or sewer backs up and causes water damage to your home, the damage won’t be covered unless you purchase this policy endorsement. Claims like these can be costly, so this extra insurance is good to have.

What type of Texas homeowners insurance policy is right for me?

The right homeowners policy for you will depend on what type of home you live in, how much it would cost to repair or rebuild, and how much your personal possessions are worth.

It often makes sense to purchase the highest level of protection you can afford — especially If you don’t have much money saved for emergencies. While a more comprehensive policy with a lower deductible will have higher premiums, it will also give you the coverage you need to get back on your feet quickly after a major loss.

As you accumulate more savings, you may be able to increase your deductible to lower your premium. However, sometimes policy pricing works out such that a $1,000 deductible may not be much more expensive than a $5,000 deductible. In that case, you’ll almost certainly be glad you paid a bit extra if you ever have to file a large claim.