How to Save Money on Home Insurance

Mortgage payments, HOA fees, property taxes, general maintenance…there are a lot of costs associated with being a homeowner. Among them includes the cost of homeowners insurance. Together, these payments begin to add up quickly, but there are ways for you to save on your premium.

Many homeowners may look to forgo maintaining a homeowners insurance policy due to the price of coverage. By law, you do not have to enroll in a home insurance policy. Some homeowners, however, may be required due to the terms and conditions of your mortgage or government loan. Either way, all homeowners are encouraged to maintain a current home insurance policy to avoid paying to restore a sizable loss.

The cost of your homeowners insurance policy will pale when compared to the cost of restoring your home and possessions after a loss from a fire, for example; however, that doesn’t mean you should look for ways to save. Homeowners are afforded more viable options for saving money on premiums than many may realize. You can save through practical, minimal efforts, personalized discounts, planning, and many other methods. Before learning how you can save money on your homeowner insurance premiums, gain a better understanding of how your insurance premium is crafted by your provider.

Understanding How Homeowners Insurance Premiums are Created

The amount you pay for your homeowners insurance premium all comes down to one thing: risk. If you are a risker client for your insurer, you’ll pay more money. If you are a client with less risk, you can expect lower premium payments. But what factors do insurance providers look at when determining risks?:

- The age of your home.

- Your home’s location.

- The value of your property, your possessions, and the change in value over time.

- The number of people living within your home.

- The amount of coverage you are enrolling in.

- Personal factors including your credit score, one of the components used to determine your insurance score.

- Your claims history.

- Your deductible.

- And many additional factors.

These factors are not only assessed by your homeowners insurance provider but are also assessed differently depending on the brand you enroll with. This is because each company uses its own weights and measures and algorithms to create a premium following its standards.

Knowing how your home insurance premium is created can help you save money. Some of the factors listed above are out of the control of the homeowner, but there are still some well within. You’ll even be able to make decisions that can lower your premium while maintaining proper coverage for your home. Let’s explore your options as a homeowner for lowering your premium while maximizing your protection.

Bundle Your Home Insurance Policy

Bundling is one of the most effective tools homeowners have at their disposal for lowering their homeowners insurance premiums. When you bundle your home insurance with an auto insurance policy or an umbrella insurance policy, you’ll find that your insurance company will deliver savings for your loyalty.

When you bundle your insurance policies, you are also gaining more than just a discount for your coverage. Insurance companies may drop clients who submit too many claims in a short timeframe. This is much less likely to happen to a client who is enrolled in multiple policies.

Take Advantage of Discounts

Beyond bundling discounts, many insurance providers offer a variety of home insurance discounts for their clients. As a homeowner, you may be surprised by how many discounts are at your disposal. Everything from your lifestyle, age, method of payment, and even affiliations with certain groups can qualify you for savings. Learn more about some of the available discount options you may be able to use to save money while retaining your homeowners insurance coverage:

- Electronic payments and paperless billing discounts are a great way to help the environment and receive savings. The cost of overhead and materials can add up for companies with a large number of clients. When customers enroll in paperless billing, your insurance provider may pass these savings onto you by discounting your coverage.

- Older homeowners may receive a discount when enrolling. Most age-related discounts apply to homeowners who are not seen as much of a risk and are at least 55 years of age.

- First-time homeowner discounts apply to new homeowners looking to purchase a home. There are plenty of costs associated with homeownership, but there are even more when purchasing a home. Closing costs may include your homeowners insurance policy, and saving money here can help you mitigate the high costs associated with purchasing your home.

- Military discounts provide those who serve us in the Armed Service with a discounted rate for their coverage. The qualifications for your discount may vary from brand to brand, but military discounts are typically available for both active military and veterans.

- Occupational and alumni discounts are provided for certain groups with organizational ties. Some alumni and companies have established relationships with insurance providers and members can receive a discounted rate as a perk.

- Non-smoking discounts can lower your home insurance premium. Although accounting for some of the rarest forms of claims, fires also cause some of the most costly claims for insurance providers. According to the U.S. National Park Service, cigarettes and other smoking materials cost almost 1,000 people their lives as the number one source of house fires in America. Property damage and liability claims caused by smoking can skyrocket and insurance providers enjoy rewarding non-smokers for lowering their risk of fire.

- Discounts for paying your homeowners insurance premium in full may also apply. Companies often reward customers which pay in full by lowering their overall premium versus customers who pay monthly. If you are financially capable of putting up the full amount for your coverage in a lump sum, you may save money in the long run.

Every homeowner is different and because of this, the factors surrounding their protection will also differ. Similarly, the same can be said about homeowners qualifying for the right home insurance discount. You’ll likely find a discount that fits your specific lifestyle may also differ from that of your neighbor. Different insurance brands may also offer different home insurance discounts. It is important to ask an agent about potential discounts you may qualify for to understand your best course of action.

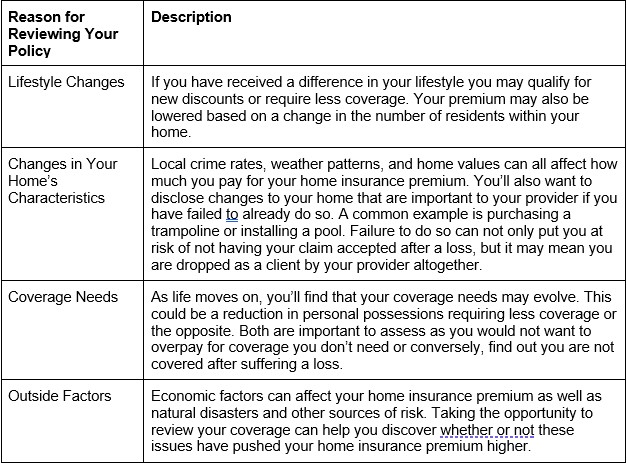

Periodically Review Your Homeowners Insurance Coverage Needs

Homeowners overspend on homeowners insurance coverage every year by failing to review their coverage. There are many reasons why reviewing your coverage can help you save and by doing so the right way, you can save hundreds if not thousands of dollars. Some of the reasons you should review your coverage are as follows:

Control the Personal Factors Which May Raise Your Rate

Reviewing your home insurance coverage takes time, but with the right agent, you’ll be able to do so in a painless manner and save money in the process. You’ll also gain peace of mind knowing that you are receiving the best coverage available for the lowest price possible.

There are some actions you can take to lower the amount you pay:

- A higher credit score can help you lower your insurance score which in turn lowers your home insurance premium. Maintaining a healthy credit score can help you save in more ways than one.

- Your claims history is a consideration and by forgoing a smaller claim, you can avoid a rate increase from your provider.

- Avoid home features such as pools or trampolines which cause your premium rates to increase.

Not everything is going to be within your control, but that’s okay. By taking care of your end, you can still lower your premium with savings that add up.

Add Safety and Security Features to Your Home

Homes with features that reduce risks against perils can receive discounts on their protection. For example, if you were to install a security system, you’ll lower your risk of a break-in. As many as 60% of burglars are deterred from homes that are cased and possess a security system. Theft and vandalism are perils covered by standard home insurance policies. By reducing this threat, insurance providers may consider your home as less of a risk to insure.

The same is true of fire detectors and smoke alarms. Fires and smoke can cause severe losses which result in expensive claims. Homeowners may also reduce their premiums by installing carbon monoxide detectors. Keeping your property and loved ones safe is its own reward, but you’ll also save more of your money on premium.

Include Home Features Which Protect Against Natural Disasters

Protecting your family and personal property from the weather is one of the primary functions of your home. Even when perils that are not covered by a homeowners insurance policy, such as a flood, affect your property, you can expect your rates to go up.

Year after year, we continue to see unexpected, expensive weather events affect millions of Americans. From the powerful hurricanes affecting the Atlantic and Gulf coasts to the winter storms which sweep throughout the Midwest, and the forest fires ravaging the West, there are a lot of natural disasters which may affect your home.

Here in Texas, we are no stranger to extreme weather. Everything from routine, severe thunderstorms bringing hail and wind damage to hurricanes to occasional winter storms are all threats to our homes. The end result can mean flooding, severe wind damage, and even damage to the structural integrity of your home. Adding home features that help lower the amount of damage your home may face due to weather can help you limit your risk while lowering your home insurance premium:

- Elevating your home to reduce potential flood damage.

- Reinforcing your home’s roof and other features to withstand the weight of snow or prevent wind damage. This is particularly helpful with older homes.

- Add features that can help protect your home during extreme weather such as storm shutters or plumbing made to withstand colder temperatures.

The amount you may spend on renovations can be substantial. Putting features onto your home for the sole reason of saving on home insurance premiums may not pay off depending on the cost of construction. It is always recommended to speak with your insurance agent about the discounts you may receive beforehand and to remodel or build said features with additional goals in mind.

Consider Risk Factors When Purchasing Your Home

Many of the risk factors potential homeowners consider before purchasing a home go hand-in-hand with the risks insurance companies look at when enrolling you as a customer. Waterfront property usually comes with a higher risk of flooding, which may mean higher premiums for your coverage. You’ll also note that living in an area of lower crime with security features and gated entrances is likely to lower how much you pay for your homeowners insurance. Additional risk factors, such as purchasing a home with a pool or trampoline, are considerations you’ll want to examine when looking to save money on your protection.

Raise Your Home Insurance Policy’s Deductible

Higher deductibles on average provide lower homeowners insurance premiums. Raising your deductible may mean you’ll pay more in the event of a loss, but it can save you from paying elevated premium rates in the present. Examining your deductible during your annual review is a great opportunity to best assess your needs and discover which money-saving opportunities are right for you.

Compare Your Coverage Among Multiple Insurance Brands

If there were ever an opportunity for this article to have a TLDR moment, it would be now:

There are many options to save for homeowners and also many factors. Your best bet is to compare your coverage to find the best price and savings opportunities.

The differences among insurance brands when determining risk will create discrepancies. Differing brands and personal factors surrounding your risk will mean different premium prices as no two homes are alike. Comparing the same risk factors among different insurance providers will produce a better overall picture of how much you can expect to pay for your coverage.

As a homeowner in Texas, you have plenty of options when it comes to your home insurance provider, but how do you know which one is right for you? Your ideal choice will be a reputable brand with a high financial rating, providing the coverage your home deserves for the lowest possible price.

Taking the time to compare your homeowners insurance policy between multiple brands is imperative for saving, but we realize how time-consuming this endeavor is. This is why the team at Freedom Insurance Group does it for you.

We work with 25+ top-rated insurance brands that can protect your home. Our agents do all of the dirty work for you by shopping among these providers to find the lowest possible price on the market for your coverage needs instantly! The average client that switches to Freedom Insurance Group saves 40% on their homeowners insurance premium.

Feel free to contact us by talking to one of our agents, or, enjoy a free homeowners insurance quote. Headquartered in Flower Mound, Texas, we proudly serve homeowners hailing throughout all of the state’s 254 counties!