Texas Vacation Home Insurance Costs & Coverages

What Is Vacation Home Insurance Coverage?

Vacation home insurance is a type of homeowners insurance that’s designed to cover the unique needs of a vacation home, from adverse weather (especially if your home is near the beach) to the extra risks of crime and vandalism in a home that you occupy only part-time.

If you rent out your vacation home on Airbnb or a similar service, your vacation home insurance should also include business insurance. That’s because homeowners insurance specifically excludes any damage incurred while a property is being used with the intention to make a profit (whether or not you’re actually turning a profit).

Why Do I Need Vacation Home Insurance?

Unless you keep enough cash handy to comfortably pay for major repairs or replacements on short notice, then vacation home insurance is probably a good idea for you. It spreads out your risk over a long time in the form of monthly, quarterly, or annual premiums. It’s easier to budget for these premiums than it is to have to pay out of pocket in an emergency.

In short, vacation home insurance helps you hold onto your favorite vacation spot, even in a worst-case scenario.

What Does Vacation Home Insurance Cover?

For a vacation home that’s intended for personal use only, vacation home insurance will be made up of a blend of these key parts:

- Physical damage coverage: This is exactly what it sounds like—coverage for any physical damage to your home, from fire, natural disaster, and even riots. Most policies will also cover damage to the belongings inside the home.

- Theft Coverage: Covers all or part of the cost of replacing your belongings if they’re stolen. If you rarely visit your vacation home, this type of coverage may become expensive, because the risk of crime goes up when you’re not around to monitor your property. But if you want it, it should be an option for you to buy regardless.

- Personal Liability Coverage: Covers the cost of legal representation and damages if you’re sued. Depending on the policy, this coverage can be surprisingly broad, covering everything from a legal battle with a disgruntled neighbor to the cost of medical bills if someone is injured on your property.

For a vacation home that’s used fully or partially for rental, your vacation home insurance will also need to include some or all of these types of coverage:

- Business Liability Coverage: Covers any lawsuits and legal fees you incur because of your rental business. Short-term rental businesses are especially prone to lawsuits from angry or injured guests, so this type of coverage is absolutely crucial to have.

- Commercial Property Coverage: Covers physical damage to your property and your guests’ property, both to the structure itself and to anything kept inside.

- Special coverage for any vehicles or recreational equipment you provide for your guests: It’s easy to throw in the use of recreational equipment like ATVs, boats, or jet skis to entice guests to your property, but these items are massive insurance headache. Your insurance company needs to know about any of these extras so that it can insure them properly—and so you’re not hung out to dry if there’s an accident.

Types of Vacation Home Insurance

There are two main ways to get vacation home insurance: by extending homeowners insurance coverage from your primary residence to your vacation home, or by buying a separate policy. One isn’t inherently better than the other, though extending your existing coverage may be slightly cheaper.

If you offer short-term rentals on the property, then you will definitely need to buy separate business insurance, though you may be able to arrange for your existing homeowner’s insurance to cover the property while you’re personally using it (when no guests are around and it’s not being used for business at all).

Here are a few common types of coverage for vacation homes:

- Dwelling Fire/DP-1: Dwelling insurance covers only the structure of the vacation home, not any belongings kept inside. It’s a good stopgap if you don’t think it’s worth it to pay for full coverage, but still want some protection, such as for a rustic cabin.

- Combined dwelling insurance/extended homeowners insurance: It’s possible to buy a dwelling insurance policy and combine it with your existing homeowner’s insurance. You could choose to extend liability coverage from your primary home to the vacation home. Or, since full-time theft coverage can be expensive for vacation homes, you could choose to extend theft coverage part-time, while you’re actually on the premises.

- Separate Home / Seasonal Insurance Policy: You can also choose to buy a completely separate homeowners insurance policy for the vacation home. This will work exactly like the policy you have on your full-time residence. This is an especially good option if your vacation home is in a state that your main homeowner’s insurance company doesn’t operate in.

An independent insurance agent can help you decide which one is the right fit for your situation. If you decide to offer short-term rentals on the property, independent insurance agents can also help you add business insurance coverage down the road.

How Much Does Vacation Home Insurance Cost?

The cost of vacation home insurance will depend on the value of the property and on its location. The primary factors that increase the cost include the structure’s replacement cost and its risk of fire, crime, and natural disasters.

Most vacation homes will cost between a few hundred and a few thousand dollars to insure annually.

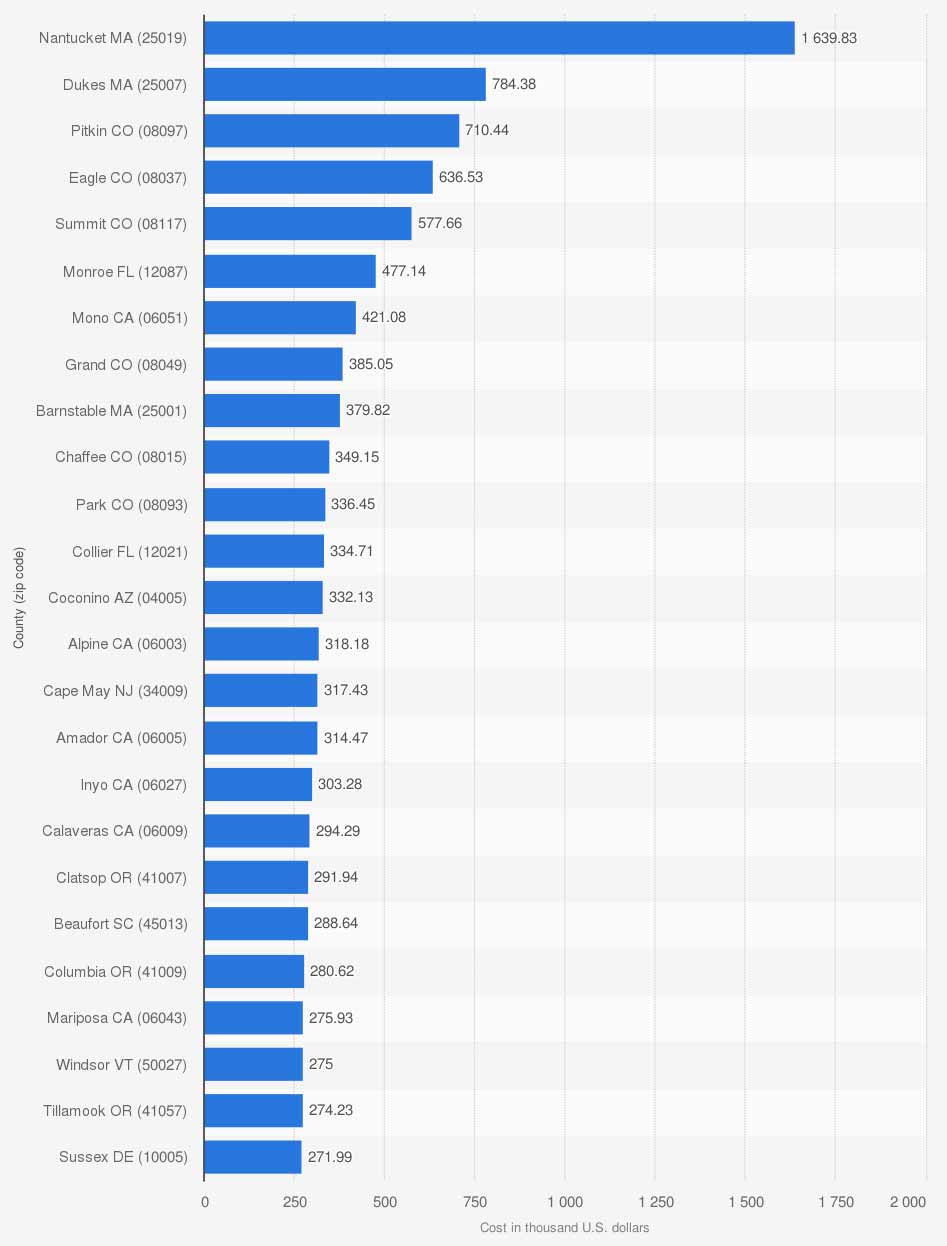

America’s Most Expensive Vacation Homes

Unsurprisingly, expensive vacation homes will be more expensive to insure, while simple, rustic properties will be cheaper. Properties in the following areas can expect some of the highest vacation home insurance costs in the nation.

The median sales price of vacation homes in selected counties in the United States in 2018 (in 1,000 US dollars)