DP-3 Policy: Home Insurance for Duplexes and Townhomes

Having a duplex, or townhome, is becoming an increasingly attractive option for homeowners. There are many benefits including a cheaper price take, fewer maintenance expenses, and depending on your situation, they can be a way to generate revenue. A DP-3 policy is one of the most popular home insurance options available for protecting a multi-family home.

But of course, that doesn’t mean it’s the only option. Different homeowners have different needs and fortunately, there are plenty of insurance products out there to meet the protection you’ll require. Explore your options and stay covered from major losses without having to overpay.

What Is a DP-3 Policy?

A DP-3 policy protects by providing coverage for a home that isn’t your primary residence. They can also protect your vacation home or duplex/townhome. These are dwelling fire policies that may not provide the same level of coverage as an HO-3 (standard home insurance) policy but can help you protect yourself against major losses.

While this is a great option for landlords throughout Texas, your tenants will need their own renters insurance to cover personal items. Landlord insurance is protection for the homeowner but if a loss afflicts your tenant’s personal property, they’ll need to restore it by other means.

Overall, DP-3 policy coverage is there to help you protect your home’s structure, your finances against liability issues, and your revenue in the event renters must leave unexpectedly and you need to maintain the income.

Homeowners Insurance or DP3 Insurance?

Ultimately, determining which policy works best for you is going to come down to where you live and your risk tolerance. By assessing your situation, you’ll be able to decide the best course of action for protecting your property and finances. Here’s a simple breakdown of DP3 vs HO3:

- If the home is a property you own but you do not live in, then your duplex or townhome can likely be protected by a DP-3 policy.

- Of course, if the duplex or townhome in question is also your residence, you’re going to want to look into an HO3 homeowners policy.

- But remember, no two situations are alike, and having a dwelling fire policy could be right for you depending on your personal variables.

- Furthermore, policies may be similar, but they are not the same. Depending on your needs and the carrier you choose, the exact coverage you receive can vary. For example, receiving coverage for your roof, loss of rental income, or liability protection on perspective coverages.

The latter is exactly why as informative as your research may be, you’re going to do best when you work with an insurance agency that has your best interest at heart. Preferably, one that works with multiple providers.

There are several reasons to shop around for your coverage, and this includes finding the right coverage for unique situations that arise when covering homes that are not traditional single-family structures.

At Freedom Insurance Group, we work with over 25 top-rated insurance providers allowing our clients access to more coverage options for their needs. This includes DP 3 coverage or standard HO-3 policies for your property.

Because we represent so many different brands, we are able to shop your coverage among trusted companies and deliver the right coverage at the lowest price, consistently. Speaking with an agent can help guide you to the right coverage.

Breaking Down DP3 Insurance

When it comes to having a DP-3 policy, this is but one option landlords have at their disposal. But there are multiple policies that offer similar coverage. However, when you look at these options, note that a DP3 is going to offer the most comprehensive coverage for landlords:

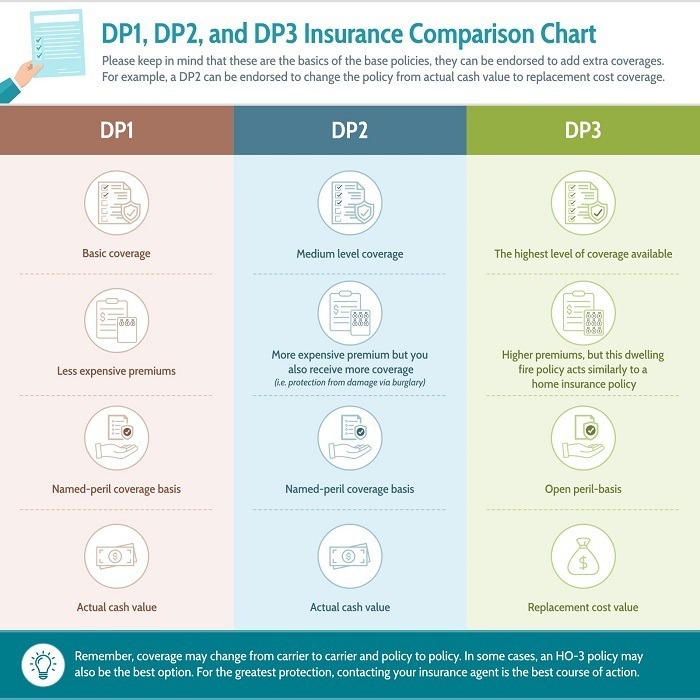

- An DP-1 policy is the most basic policy you can enroll in as a landlord. Offering dwelling fire coverage, you’ll be protected from losses on a named peril basis. In other words, to receive reimbursement, you’ll need to have the peril named on your policy.

- DP2 insurance is going to be a step up from the DP1. Again, you’ll receive coverage under a named peril basis, however, you’ll receive protection against more perils that your duplex or townhome may face.

- DP3 is the most common protection and offers the best amount of coverage for dwelling fire insurance. You’re protected on an open peril-basis and this coverage is the closest to a home insurance policy of the three.

When comparing a DP1 vs DP3 policy, you’ll need to understand that while you’ll receive more with a DP-3 dwelling policy, you’re also going to have to pay more in premiums. Furthermore, both DP1 and DP2 coverages use actual cash value (ACV) when reimbursing policyholders whereas DP3 policies use replacement cost value (RCV).

DP1 DP2 DP3 Insurance Comparison Chart

DP 3 Policy Exclusions

Just as a home insurance policy isn’t blanket coverage, neither is a DP-3 policy. You’re going to find that there are several things not included in your protection. For example:

- Flood damage is going to need a separate flood insurance policy.

- Damage from vandalism/burglaries may be covered but it depends on your policy.

- You’re also going to want to understand building codes. If you need to upgrade your place to stay in sync with Texas laws, you’ll have to do so out-of-pocket without the right coverage.

- It’s also important to remember that personal property can be an issue, but if you’re a landlord, your tenants will need their own coverage.

Can My Insurance Company Cancel My DP-3 Policy?

Yes, your insurance company can cancel your DP-3 policy for a number of reasons, but in most cases, this isn’t an issue. Here’s what you’ll want to avoid:

- Insurance fraud should be an obvious thing to avoid, but even accidentally leaving off information can land you in trouble. For example, if you decide to put in a swimming pool and fail to notify your insurance carrier, you may find a claim denied in the future or even yourself dropped as a client.

- You can also be dropped as a client through non-renewal. It’s important to note that this is not the same as having your policy canceled, however, but rather a carrier deciding not to continue on with you as a client passed your current insurance policy.

Does a DP-3 Policy Cover Damages Done From Theft?

Yes, your DP3 coverage protects against theft, though policy limits will apply. Furthermore, it’s important to remember that a tenant’s personal property requires a separate policy. There are some allowances for personal property that is used to maintain the property that can be covered that belong to you as a landlord.

How To Protect Your Duplex or Townhome in Texas

Your home is unique and so too should be your protection. There are a number of scenarios that can come with protecting any property and duplexes/townhomes are often even more complex. Finding affordable coverage doesn’t need to be a hassle and our agents can help.

All homeowners are looking for the same thing, protection for their homes at the lowest price possible. We’ve been helping Texans find these coverage options since 2005.

There are many factors that companies use to create your premiums, but even as similar as these variables are, the way they have assessed ranges from brand to brand. Because of this, you’ll notice that even the same exact coverage will vary greatly in the price you’ll have to pay.

Comparing your coverages helps you sort through the noise and find the lowest price. It also helps homeowners/landlords protect better with an appropriate policy for their needs.

Freedom Insurance Group is here to do the dirty work for you. Save more by contacting our agents today, or get a free home or landlord insurance quote online. From an HO-3 policy to a DP-3 policy and more, we can help you find the right coverage for less.